IRS Notices

IRS CP21A Notice: We Changed Your Return and You Owe (2026)

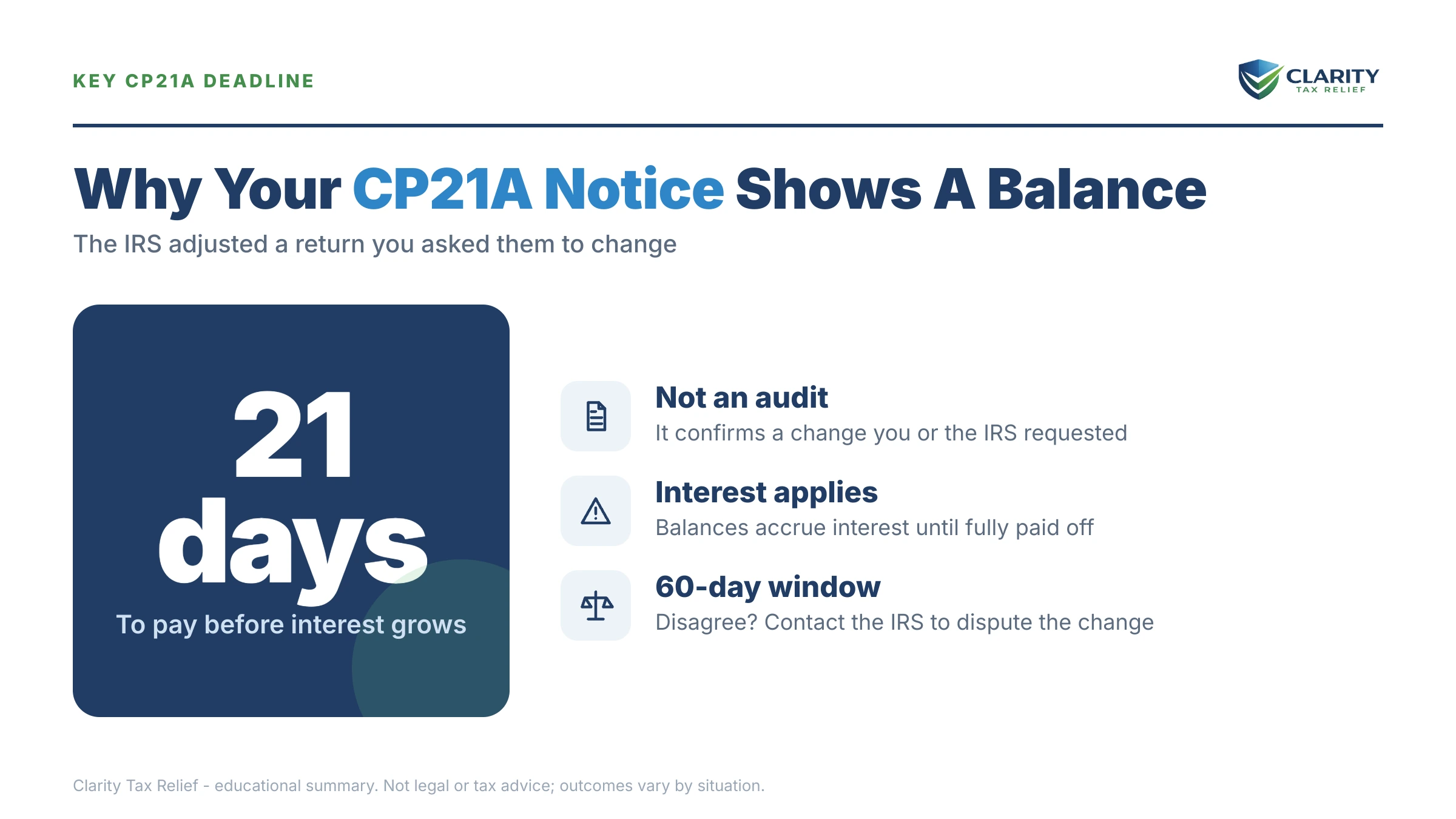

The short answer: a CP21A notice means the IRS made the changes you requested — usually after processing a Form 1040-X amended return — and the recalculation left a balance due. Pay or set up a payment arrangement by the date printed on the notice, typically about 21 days, before the balance enters the IRS collection sequence.

You amended your return to fix a mistake — and months after mailing the 1040-X, the IRS finally answered. The odd part: the CP21A notice confirms your correction went through exactly as you asked, then bills you more than you calculated when you filed it. That gap isn't an error, and this page explains where it comes from and what to do about it.

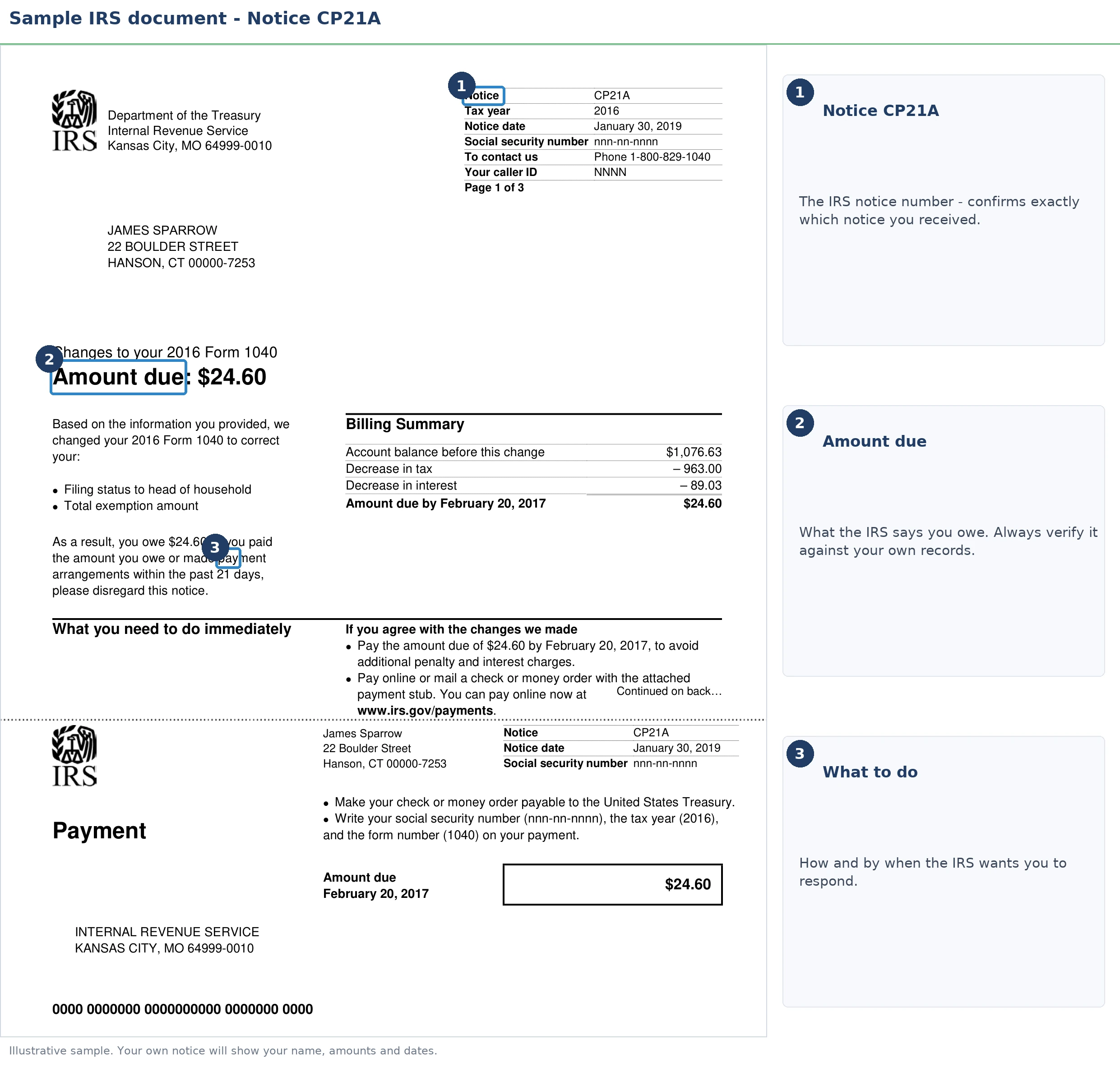

Here's the map: verify the numbers match your amendment, understand why interest is backdated, then pay or arrange payment before the printed date. The image below shows exactly what a CP21A looks like and where to find the three numbers that matter — the change to your tax, the interest added, and your pay-by date.

⏱ Your deadline: the pay-by date printed on your CP21A — typically about 21 days from the notice date. Interest and the 0.5% monthly failure-to-pay penalty keep accruing on the new balance after that date, and the IRS's automated system starts queuing reminder notices.

Why you got a CP21A notice

A CP21A notice means the IRS adjusted your tax return at your own request — most often after processing a Form 1040-X amended return — and the change resulted in money owed. Unlike almost every other balance-due letter, this one exists because of something you initiated.

The most common triggers: you amended to add income you forgot (a late-arriving 1099, a second W-2), you removed a credit or deduction you realized you didn't qualify for, or you asked the IRS in writing or by phone to correct something on your account. The notice shows the tax year, the adjustment, and the new balance broken into tax, penalties, and interest.

Two things a CP21A is not. It is not an audit — nobody is examining your return; the IRS did what you asked. And it is not a surprise assessment the IRS invented — if you never requested any change, that itself is the red flag, and you should call the number on the notice before paying anything. For the broader question of how IRS letters work in general, start with why did I get a letter from the IRS; everything below is specific to the CP21A.

CP21A vs. the rest of the CP21/CP22 family

The IRS uses five closely related notices for return adjustments, and the last digit changes everything. If your letter isn't exactly a CP21A, you're on the wrong page — here's the family at a glance:

| Notice | What changed | Result |

|---|---|---|

| CP21A (this guide) | Changes you requested, usually via Form 1040-X | You owe money |

| CP21B notice | Changes you requested | You're due a refund |

| CP21C notice | Changes you requested | No balance due either way |

| CP21E notice | Changes from an audit or examination | You owe money |

| CP22A notice | Changes made from information you provided | You owe money |

One more distinction worth knowing: if the IRS changed your return without you asking — because of a math or clerical error it caught on its own — you'd have received a CP11 notice (balance due) or a CP12 notice (refund changed) instead. Those carry different dispute rights, so the notice number matters.

Why the CP21A balance is bigger than your 1040-X said

Interest on a CP21A balance runs from your return's original due date — not from the day you amended, and not from the notice date. That single rule explains the most common CP21A shock: you calculated the extra tax on your Form 1040-X, but the bill that arrives is noticeably larger.

Amended returns are processed by hand and routinely take months. Every one of those months added interest, plus the failure-to-pay penalty of 0.5% per month on the unpaid tax. So a correction you filed in the spring can arrive as a CP21A in the fall carrying nearly a year of statutory additions — even though you did the responsible thing by amending. If your 1040-X is still pending and you haven't received the CP21A yet, our guide on where's my amended return covers the processing timeline.

If you sent a payment with your 1040-X, check your IRS online account before paying again — payments frequently post before the notice is generated, or land in the wrong tax year. To estimate how the interest and penalty on your own balance were built — and what continues to accrue while you decide — you can run the numbers through our Penalty & Interest Calculator.

What happens if you ignore a CP21A

An unpaid CP21A enters the same automated collection stream as any other IRS bill — a stream that ends in bank levies and wage garnishment, not just letters. The sequence runs on autopilot: IRS staffing fell roughly 27% in 2025, but the notice system and levy programs are automated and never paused. Ignoring the mail doesn't mean a human forgot about you.

- CP21A — the bill for the adjustment you requested. No enforcement power. This is the cheapest moment to resolve it.

- CP501 / CP503 — reminder notices. Still just bills, but interest and the monthly penalty compound the whole time.

- CP504 notice — Notice of Intent to Levy. The IRS can now take your state tax refund, and a federal tax lien becomes a realistic next step.

- LT11 notice / Letter 1058 — Final Notice of Intent to Levy. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After 30 days, the IRS can levy bank accounts and garnish wages.

If you rent rather than own, don't assume there's nothing to take. Levies don't need real estate: a bank levy freezes the funds in your account with a 21-day hold before the money leaves, and a wage levy attaches to every paycheck continuously until it's released. For a renter, the paycheck and the checking account are exactly what the IRS reaches first.

| Notice | Your window | What you lose if it passes |

|---|---|---|

| CP21A | The pay-by date printed on the notice (typically ~21 days) | The cheapest resolution — penalty and interest compound and reminders begin |

| CP501 / CP503 | Pay or arrange payment on receipt | Nothing formal yet, but the balance keeps growing monthly |

| CP504 | Act before the levy date on the notice | Your state tax refund; a federal tax lien becomes likely |

| LT11 / Letter 1058 | 30 days to request a hearing on Form 12153 | Your pre-levy Collection Due Process hearing — then bank and wage levies can begin |

Holding a CP21A right now?

Send us a photo of it along with your 1040-X. An experienced tax professional will confirm the IRS applied your amendment correctly and map your cheapest path to zero — free, before the pay-by date on your notice passes.

Your options if you can't pay the CP21A in full

The IRS has several payment programs for a CP21A balance, and most people who amended a return qualify for the simplest ones. The notice presents only "pay now" — here is the full menu, with what each actually costs:

| Option | Eligibility at a glance | Upfront cost | What to know |

|---|---|---|---|

| Pay in full | Anyone | $0 | Stops the penalty clock and the notice sequence immediately |

| Short-term plan | Can pay within 180 days | $0 setup fee | Interest and the 0.5%/month penalty continue, but escalation stops |

| Installment agreement | Balances ≤ $50,000 set up online, up to 72 months; ≤ $10,000 may qualify as a guaranteed installment agreement | Setup fee (lowest with direct debit; waived for qualifying low-income taxpayers) | Interest continues; missing a payment risks default |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses | $0 | Collection pauses; the debt and interest remain and the IRS reviews periodically |

| Offer in Compromise (Form 656) | Assets plus future income genuinely can't cover the debt before the collection statute expires | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | The IRS accepted roughly 1 in 5 offers in FY2024 — a math test, not a negotiation |

| Penalty relief | Clean compliance history for the prior 3 years, or a qualifying reasonable cause | $0 | Removes penalties, not the tax or interest; see first-time penalty abatement — and starting summer 2026, the Automatic Exemption from Penalty applies some relief with no request at all |

A worked example: a $7,400 CP21A

Say you amended your return to add a 1099 you forgot, and the CP21A arrives showing $7,400 — roughly $6,800 in additional tax plus about $600 in backdated interest and failure-to-pay penalty from the months your amendment sat in processing. You rent, you have no savings cushion, and you can't write that check. Here's the realistic math:

- Short-term plan (180 days): $7,400 ÷ 6 ≈ $1,235/month. No setup fee, but a heavy monthly hit — this fits only if the money is genuinely coming (a bonus, a tax refund next spring).

- 72-month installment agreement: $7,400 ÷ 72 ≈ $103/month before ongoing interest — budget modestly above that. Because the balance is under $10,000, the guaranteed installment agreement rules generally apply if you've filed and paid on time for the past several years and can pay it off within three years.

- Offer in Compromise: usually the wrong tool at this size. With steady wages, the IRS's own formula will typically show it can collect $7,400 over 72 months — meaning an offer for less would be rejected on the math alone.

For most people holding a four-figure CP21A, a payment plan set up before the pay-by date is the whole solution — and the levy sequence above never begins.

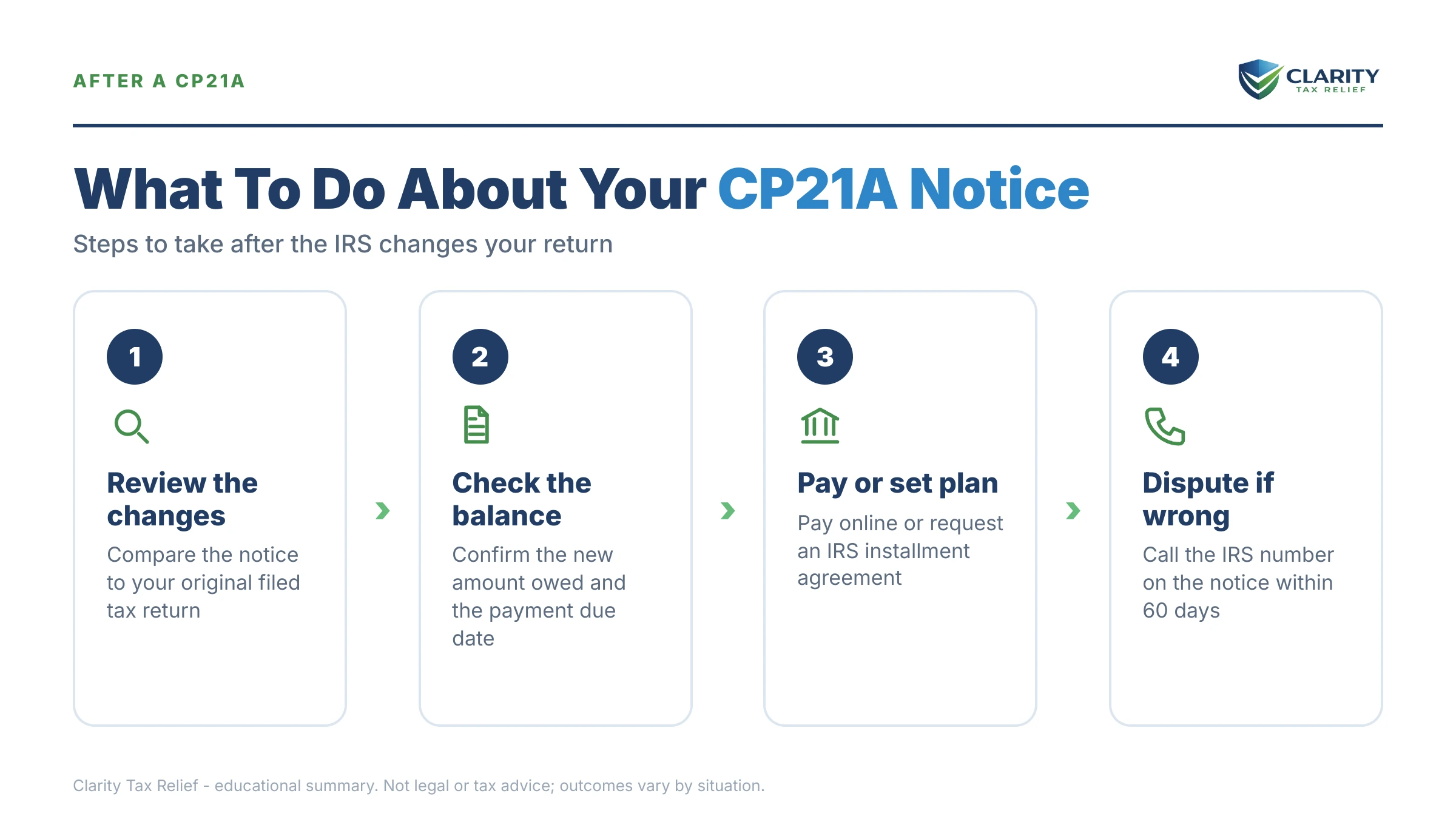

How to respond to a CP21A, step by step

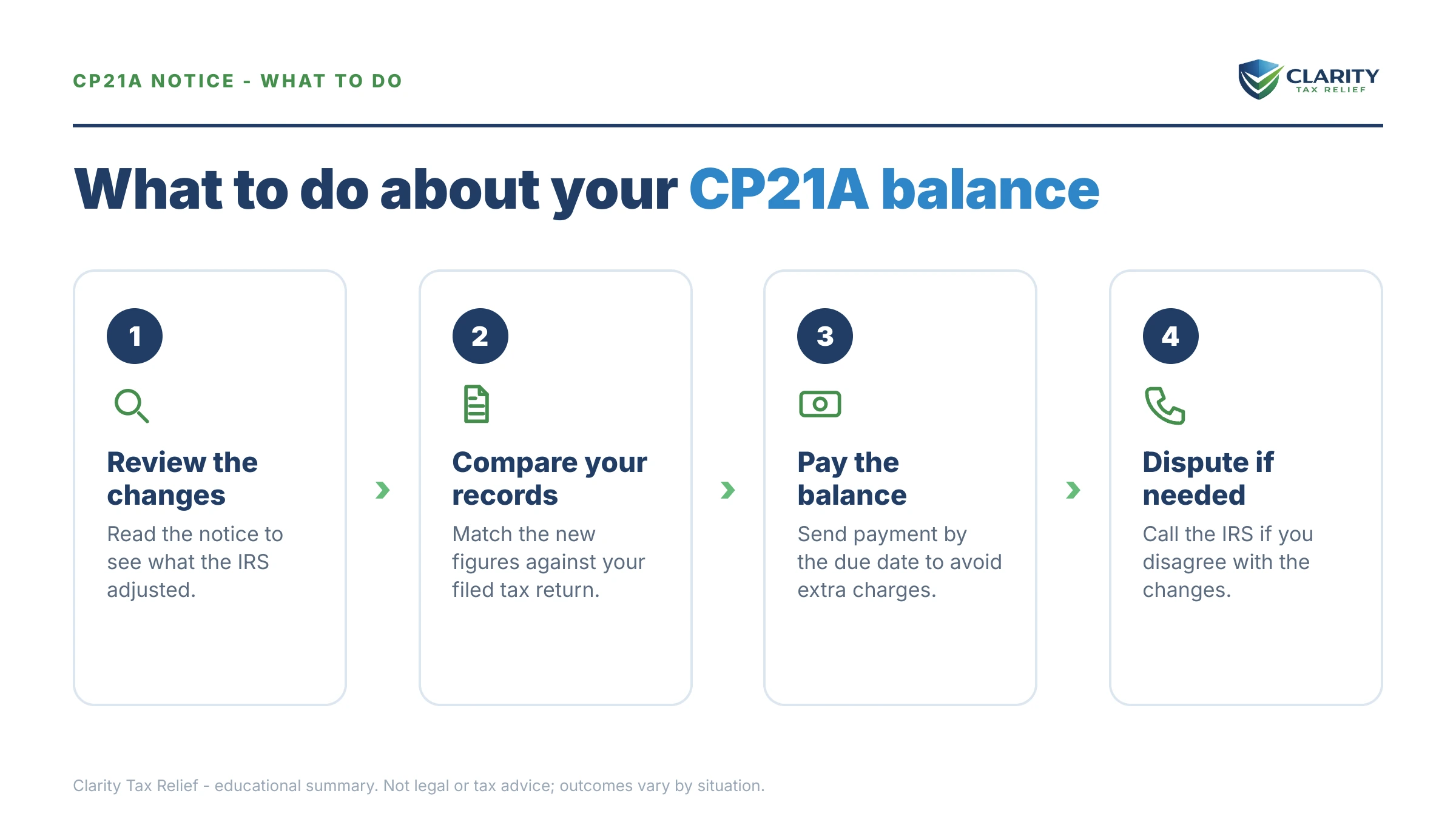

- Compare the notice to your amended return — Pull your Form 1040-X copy and match the "changes we made" section of the CP21A line by line against what you filed.

- Verify the balance online — Log in to your IRS online account and confirm the new assessment — and any payment you already sent — posted to the correct tax year.

- Pay by the notice date if you can — Pay at IRS.gov/payments to stop the failure-to-pay penalty from compounding and keep the balance out of the collection sequence.

- Set up a payment arrangement if you can't pay in full — Choose a short-term plan or installment agreement before the pay-by date — an arrangement in place stops the escalation even though interest continues. Details on every plan are on the IRS payment plans page.

- Dispute in writing if the numbers are wrong — Call the number on the notice or respond in writing with your 1040-X copy and proof of any payment, and keep copies of everything you send.

The IRS's own summary of this notice is at Understanding your CP21A notice — worth a skim to confirm the letter you're holding matches the real thing.

When you can handle a CP21A yourself

Most CP21A notices don't require professional help — you triggered the change, so you usually already know the balance is correct. Handle it yourself if the notice matches your 1040-X, the balance is one you can pay within 180 days, or a simple online payment plan covers it. Setting up a plan on a correct four-figure balance is a 20-minute task, not an engagement.

Experienced help changes the outcome in a narrower set of situations: the CP21A doesn't match what you filed and phone attempts have gone nowhere; you have multiple amended years or other unpaid balances stacking behind this one; a CP504 or LT11 arrived while your amendment was processing, meaning enforcement is already in motion; or penalties make up a large slice of the balance and an abatement request could remove them before you pay. In those cases, the order you fix things in — dispute, penalties, then the balance — changes what you ultimately pay.

Terms on your CP21A, decoded

- Amended return (Form 1040-X): the form used to correct an already-filed tax return — the usual trigger for a CP21A.

- Assessment: the formal recording of your new balance on the IRS's books, which is what makes it legally collectible.

- Statutory interest: interest the law requires the IRS to charge, running from the return's original due date until the balance is paid.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month, added on top of interest until you pay or qualify for relief.

- Levy vs. lien: a levy takes property (bank funds, wages); a lien is a legal claim against property — a levy is the one that touches a renter's paycheck.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though certain events pause that clock.

CP21A questions, answered

Why did I get a CP21A notice from the IRS?

Because the IRS made a change to your return that you requested — most commonly by filing a Form 1040-X amended return — and the recalculation shows a balance due. It can also follow a written or phone request to correct something on your account. If you never asked for any change, call the number on the notice: a CP21A should never arrive unprompted, and an unexpected one can signal a processing error or identity problem.

How long do I have to pay a CP21A?

Pay by the date printed on the notice — typically about 21 days from the notice date. Interest and the 0.5% monthly failure-to-pay penalty keep accruing after that date, and the balance feeds into the IRS's automated reminder sequence. If you can't pay in full by the date, setting up a payment arrangement before it passes stops the escalation even though interest continues.

What if I disagree with the amount on my CP21A?

Call the number on the notice or respond in writing with your copy of the amended return and any payment confirmations. Amended returns are processed by hand, and transcription errors — a credit missed, a payment posted to the wrong year — do happen. Don't pay a figure you can document is wrong; send proof, keep copies of everything, and confirm the correction posts to your IRS online account.

What is the difference between a CP21A and a CP22A?

Both say the IRS changed your return and you now owe money — the difference is the paper trail behind the change. A CP21A typically follows an amended return or a correction you directly requested, while a CP22A covers adjustments the IRS made based on information you provided. The response playbook is the same for both: verify the change against your records, then pay or arrange payment by the printed date.

Is a CP21A notice an audit?

No. A CP21A is a bill that confirms a change you asked for, not an examination of your return. Nobody is questioning your deductions or requesting documents. Audits arrive through entirely different letters and follow a different process with formal appeal rights. The only risk a CP21A carries is the balance itself — which grows and eventually reaches enforcement if it goes unpaid.

Why does my CP21A include interest from months ago?

Because interest on additional tax runs from your return's original due date — not from the day you amended, and not from the notice date. Amended returns can take months to process, and interest accrued through that entire wait. That's why the CP21A total is often noticeably larger than the extra tax you calculated on your Form 1040-X.

Can a CP21A lead to a wage or bank levy?

Not directly — a CP21A carries no enforcement power by itself. But an unpaid CP21A balance enters the same collection stream as any IRS debt: reminder notices, then a CP504, then an LT11 final notice that starts a 30-day clock before the IRS can levy bank accounts and garnish wages. Renting instead of owning doesn't protect you — levies reach paychecks and bank accounts, not just property.

I sent a payment with my amended return — why does the CP21A still show a balance?

Your payment may have crossed in the mail with the notice, posted to the wrong tax year, or not yet been applied when the CP21A was generated. Log in to your IRS online account and check whether the payment shows for the correct year. If it posted, the remaining balance is usually just the interest and penalty that accrued during processing. If it didn't post, respond with your payment confirmation rather than paying twice.

Your next 24 hours

- Find two things on the notice: the pay-by date near the top, and the "changes we made to your return" section that breaks the balance into tax, penalty, and interest.

- Gather three documents: your Form 1040-X copy, the original return for that year, and confirmation of any payment you sent with the amendment.

- Get a free CP21A review: use the 2-minute form or call (888) 825-7779. An experienced tax professional can confirm the numbers and set the right arrangement before your pay-by date passes — while the balance is still a bill, not a collection case.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.