IRS Notices

IRS CP22E Notice: Audit Changes From Exam and What to Do (2025)

The short answer: a CP22E notice is the bill the IRS sends after an examination — an audit — changed your tax return and left you with a balance due. The new amount, plus penalties and interest, is printed on the notice. You generally have about three weeks from the notice date to pay or set up a payment arrangement.

Holding a CP22E right now?

Send us a photo of it. An experienced tax professional will decode exactly what the audit changed, whether it can be challenged, and what your options are — free, confidential, no pressure.

⏱ Your deadline: the "pay by" date printed on the notice — typically 21 days from the notice date (10 business days if you owe $100,000 or more). Interest and the monthly failure-to-pay penalty keep adding up after that date, and the IRS's automated collection notices start arriving.

Why you got a CP22E

The IRS examined one of your tax years and made changes that increased what you owe. The "E" stands for examination. By the time a CP22E reaches your mailbox, the audit is closed, the IRS has officially assessed the extra tax, and this notice is the resulting bill. The IRS's own explainer is at Understanding your CP22E notice.

Common reasons an exam ends with a balance: deductions or credits the IRS disallowed because they weren't substantiated, income the IRS added back, or an adjustment to your filing status or dependents. The notice shows the tax year, the new balance, and how it breaks down between tax, penalties, and interest. Sometimes a CP22E follows an in-person or mail audit; other times it follows an audit report (Letter 525) you may have already received.

What happens if you ignore it

A CP22E doesn't expire, and the collection process that follows is automated. Ignore each notice and the next one shows up roughly five weeks later, with more interest attached and more enforcement power behind it:

- CP22E — the bill from your exam. You are here. No enforcement yet.

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows monthly.

- CP504 — Notice of Intent to Levy. The IRS can seize your state tax refund, and a federal tax lien becomes a real possibility.

- LT11 / Letter 1058 — Final Notice. After 30 days the IRS can garnish wages and levy bank accounts. You have formal appeal rights here — but far fewer good options than you have today.

The system keeps moving whether or not you agree with the audit. Acting now, while this is only a bill, keeps every door open.

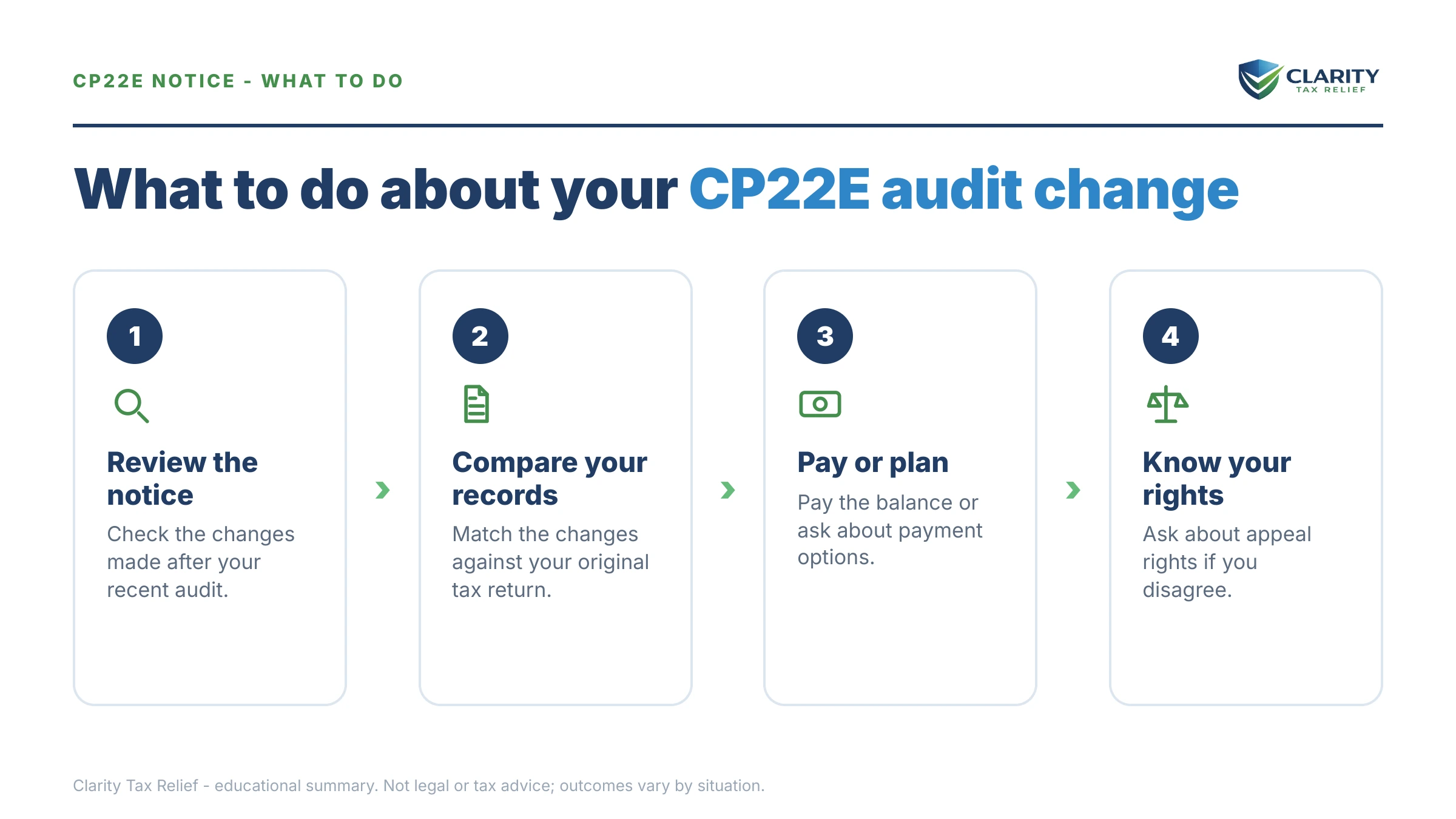

First: make sure the CP22E is actually right

Audit adjustments aren't always correct, and they aren't always final. Before you pay anything, spend a little time checking:

- Read the changes line by line. The notice (and the exam report behind it) should explain exactly what the IRS adjusted and why. Compare it to your return and your records.

- Log into your IRS online account to confirm the balance and check for recent payments that may have crossed in the mail.

- Ask yourself whether you ever made your case. Many exam changes happen because the taxpayer didn't respond, didn't send documents, or never knew the audit was open. If that's you, the adjustment may be reversible.

- Screen for scams. A real CP22E arrives by postal mail, never email or text. Real IRS payments go only to the United States Treasury or through IRS.gov — anyone demanding gift cards, wire transfers, or payment apps is a criminal, not the IRS.

If you disagree with the audit changes

If you have records the IRS never saw, you can request audit reconsideration — you send the documents you didn't provide the first time, and the IRS reviews whether the assessment should change. See the IRS overview at IRS audit reconsideration. You generally need to stay current on the account while it's being reviewed.

Reconsideration works best when you can show new information that wasn't considered. If you already signed a form agreeing to the audit results, your options narrow — but they don't always disappear. In some cases amending the return or pursuing innocent-spouse relief still helps. This is a good moment to have an experienced tax professional read your file before you commit to anything. The Taxpayer Advocate Service, an independent organization inside the IRS, can also help when you're stuck — see the Taxpayer Advocate Service.

If you can't pay in full: your real options

The notice offers two choices — pay or else. In reality the IRS has several programs, and which one fits depends on your finances:

- Short-term payment plan — up to 180 extra days to pay in full. No setup fee. Interest and penalties continue, but enforcement stops.

- Installment agreement — a monthly payment plan (details on the IRS payment plans page). For balances under about $50,000, "streamlined" agreements can usually be set up without detailed financial disclosure, spread over up to 72 months.

- Currently Not Collectible status — if paying anything would create genuine hardship, collection can be paused while your situation improves. The debt remains, but garnishments and levies stop.

- Offer in Compromise — settling for less than the full balance. It's real, but only when your assets and income genuinely can't cover the debt; the IRS runs the math, not the marketing. Anyone promising to settle for pennies on the dollar before reviewing your finances is selling you something. An experienced tax professional can tell you whether you're actually a candidate before you spend anything pursuing it.

- Penalty relief — if this is your first slip in years, first-time penalty abatement can remove the failure-to-pay penalty entirely. Reasonable-cause relief may apply for illness, disaster, or other circumstances beyond your control.

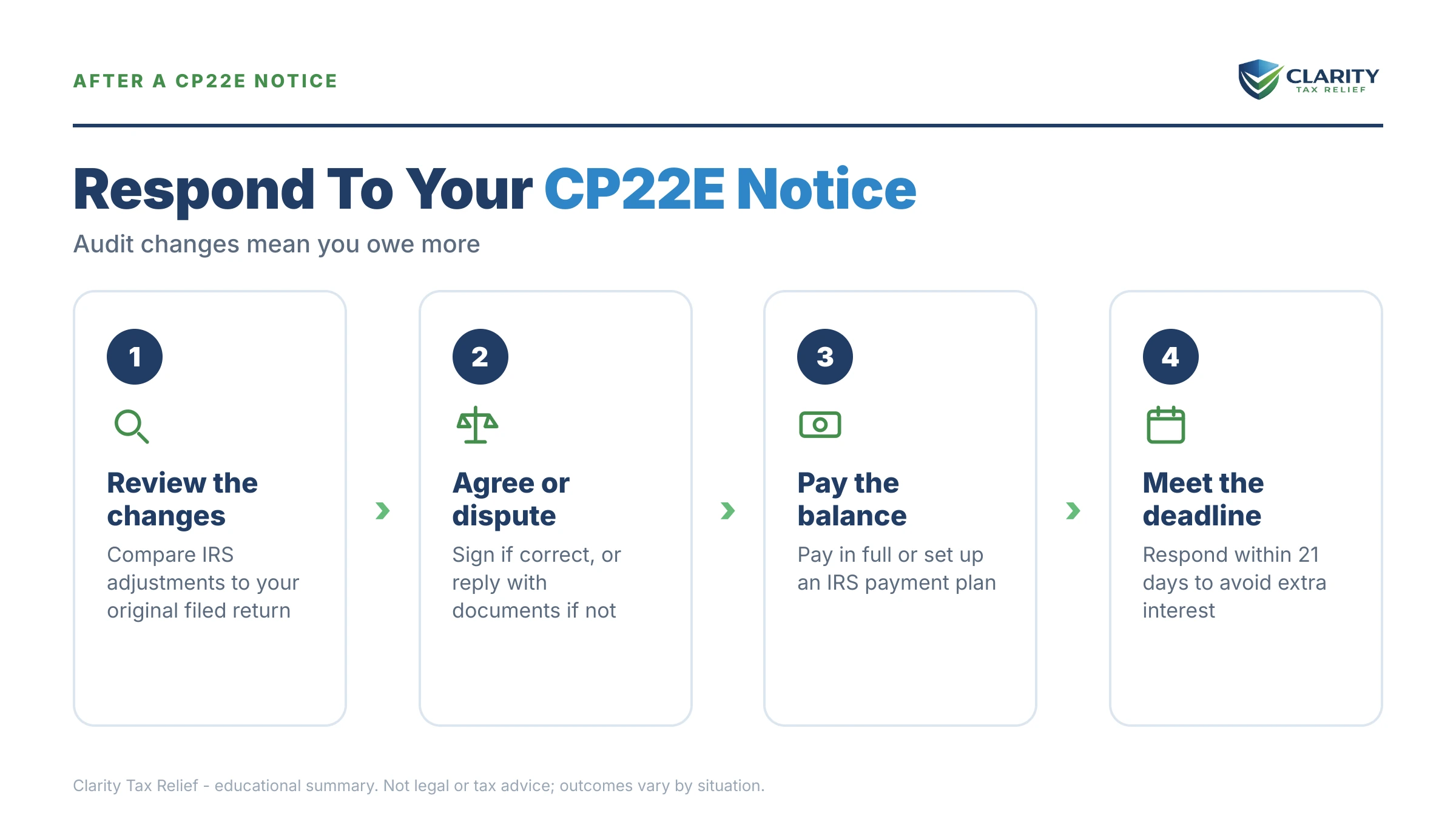

How to respond to a CP22E, step by step

- Verify the changes against your return, your records, and your IRS online account (see above).

- If you disagree and have proof: request audit reconsideration with copies of the documents the IRS didn't consider, and keep copies of everything.

- If it's correct and you can pay: pay by the notice date at IRS.gov/payments — that stops penalties and the notice sequence immediately.

- If you can't pay in full: pick the option above that fits and set it up before the deadline. Even a plan you start today prevents everything that follows.

- If you owe more than $10,000, have other open years, or just want it handled: get a professional review first — the order you fix things in (dispute, penalties, then the balance) changes what you end up paying.

CP22E questions, answered

Is a CP22E notice an audit?

The audit already happened. A CP22E is the bill that comes after an IRS examination made changes to your return. By the time it arrives, the exam is closed and the IRS has assessed the additional tax, penalties, and interest. It's a collection notice, not a new audit.

What can I do if I disagree with my CP22E?

If you never got to make your case during the exam, you can request audit reconsideration by sending the IRS the documents and records you didn't provide the first time. You generally must keep the account current while it's reviewed. If you signed an agreement closing the audit, your options are more limited, so get an experienced tax professional to look at your file.

What if I can't pay the amount on my CP22E?

You have options the notice doesn't advertise: a short-term plan of up to 180 days, a monthly installment agreement, hardship status that pauses collection, or — when your finances genuinely qualify — an Offer in Compromise for less than the full balance. Penalty relief may also reduce what you owe.

How long do I have to respond to a CP22E?

Pay or arrange payment by the date printed on the notice — usually about 21 days from the notice date, or 10 business days if you owe $100,000 or more. After that, interest and the monthly failure-to-pay penalty keep growing and the IRS's automated collection notices begin.

What's the difference between a CP22E and a CP22A?

Both say the IRS changed your return and you now owe. A CP22A usually follows a correction you asked for or a data-matching change. A CP22E specifically follows an examination — an audit — which means appeal and reconsideration rights tied to the exam may apply to you.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.