IRS Notices

IRS CP23 Notice: Estimated Tax Payments Don't Match and You Owe (2026)

The short answer: a CP23 notice means the IRS changed your tax return because the estimated tax payments you claimed don't match the payments posted to your account — and the difference leaves you owing a balance. Before paying anything, verify the IRS's payment records: misapplied payments, not missing money, cause many CP23s.

You paid your quarterlies all year — you scheduled them, you have the bank records — and the IRS just billed you anyway. That's the specific sting of a CP23: it doesn't accuse you of underreporting income; it says one or more of the payments you counted on your return never showed up on your account. The good news is that "never showed up" very often means "posted somewhere else," and a misrouted payment can be moved.

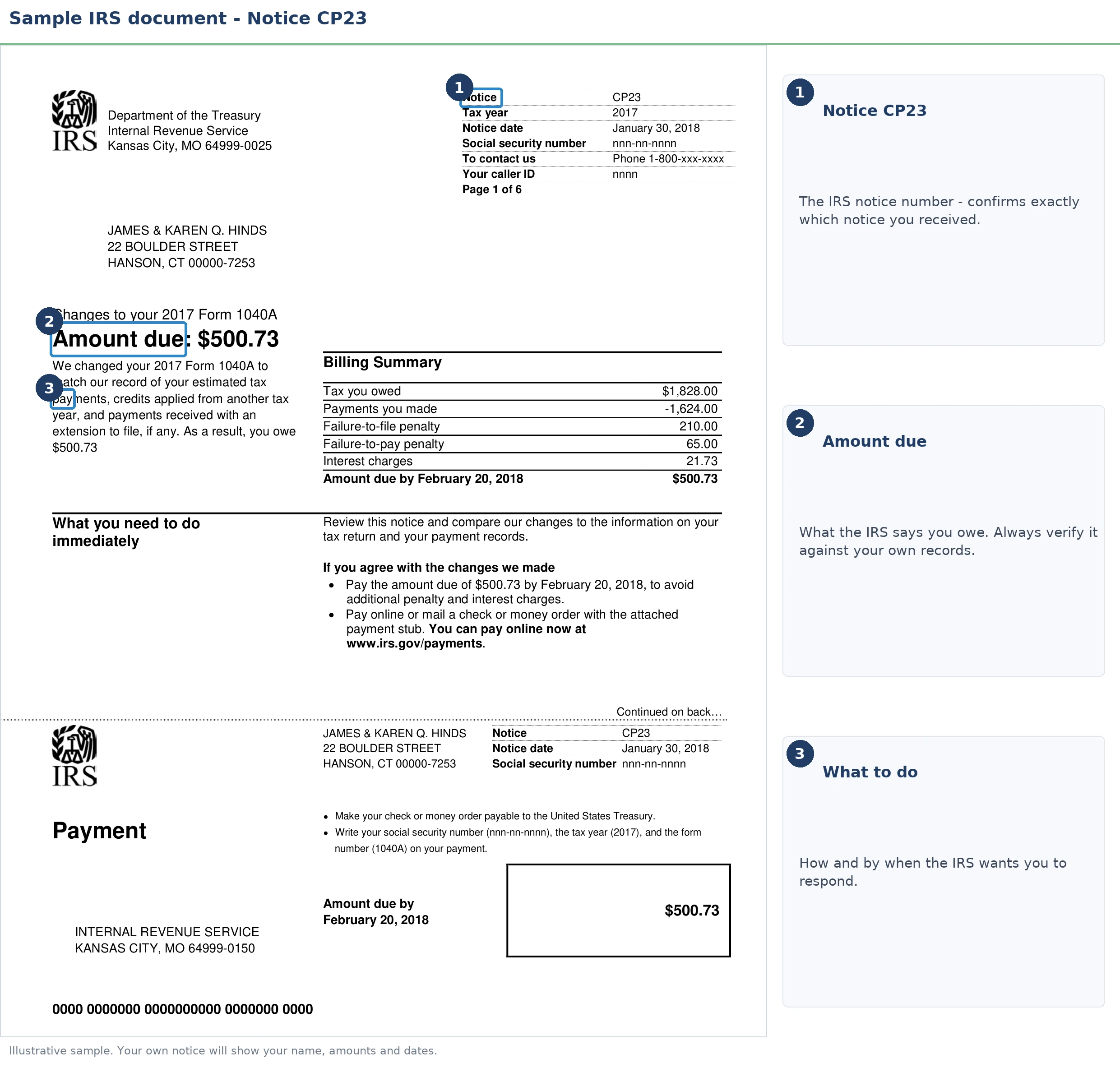

Your CP23 shows two numbers side by side: the total estimated payments you claimed and the total the IRS posted. The gap between them, plus penalties and interest, is the balance due. The image below shows exactly what a CP23 looks like and where that payment comparison sits, so you can find the figures the IRS actually used.

⏱ Your deadline: the "pay by" date printed on your CP23. Interest compounds daily and the 0.5%-per-month failure-to-pay penalty keeps running past that date. If you plan to dispute the balance, your notice states its own dispute window — start before either date passes.

Why you got a CP23 notice

The IRS sends a CP23 when the Form 1040-ES payments claimed on your return don't reconcile with its own payment records — and the correction leaves a balance due. This is an account-matching problem, not an audit. Nobody is questioning your deductions or your income; a computer compared two columns of numbers and found a gap.

Three things can be true, and your entire strategy depends on which one it is. Either the IRS misapplied a payment you actually made, you claimed a credit that never existed, or the payment failed somewhere between your bank and the Treasury. Each has a different fix, which is why the worst move is paying the notice on autopilot — and the second-worst is ignoring it while you "look into it later."

If you're not sure why the IRS is writing to you at all, or you received several letters at once, start with our broader guide to why did I get a letter from the IRS and come back here for the CP23 specifics.

First: find the payment the IRS says is missing

Most CP23 disputes are won with a payment confirmation number, not an argument. Before you pay or call anyone, pull the IRS's version of your payment history — log into your IRS online account or request an account transcript — and line it up against your own records, quarter by quarter.

Then look for one of these patterns. They account for the overwhelming majority of estimated-payment mismatches:

| What went wrong | How it shows up | The fix |

|---|---|---|

| Payment applied to the wrong tax year | Your January payment for Q4 posted to the new year, or an online payment defaulted to the current year instead of the year you meant | Ask the IRS to transfer the payment to the correct year; penalties and interest recompute once it moves |

| Payment made under the wrong SSN | Quarterlies paid from your spouse's IRS profile posted to their individual account, not to the joint return | Request the payments be credited to the joint account; provide both SSNs plus the payment confirmations |

| Prior-year overpayment that never carried forward | You elected to apply last year's refund to this year's estimates, but that refund was reduced, adjusted, or offset to another debt | Compare last year's final refund to the credit you claimed; if it was offset, that's a separate problem to trace |

| A typo on the return | A transposed figure or a quarter counted twice inflated the payments line | If the IRS's number is right, the balance stands — skip to the payment options below |

| Payment that never cleared | A check bounced or a bank debit was rejected, so the payment was reversed off your account | Confirm with your bank, re-pay promptly, and watch the mail for a dishonored-payment penalty notice |

The wrong-SSN problem deserves special attention if you're married. Estimated payments only credit automatically to the account they're paid under — so if your spouse made the quarterly payments from their own IRS profile and you filed jointly under your SSN as primary, the IRS's computers may never connect the two. Divorced or separated in the middle of a tax year? Joint 1040-ES payments can be allocated between you, but the IRS won't split them the way you expect unless someone tells it how.

If you find the missing payment, call the number printed on the top right of your CP23 with the confirmation number, date, and amount in front of you — or respond in writing with copies (never originals) of canceled checks, front and back, or your Direct Pay/EFTPS confirmations. In 2026, with the IRS workforce down roughly 27%, written responses can take months to process, so a phone correction is usually faster when you can get through. Keep notes of every call: date, time, and the employee's ID number.

What happens if you ignore a CP23

An unpaid CP23 balance enters the same automated collection pipeline as any other tax debt — the system doesn't care that the underlying cause was a payment mismatch. Each notice below arrives only if the one before it goes unanswered, and each carries more power than the last:

- CP23 — you are here. An adjusted return and a first bill. Interest and the failure-to-pay penalty are already running, but the IRS has no enforcement power yet.

- CP501 / CP503 — automated reminders that the balance remains unpaid and is growing every month.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a realistic next step. Our CP504 notice guide covers this stage in full.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts, and when it expires the IRS can garnish wages and levy bank accounts. See the LT11 notice guide for the rights that attach here.

If you rent, this sequence hits differently than it does a homeowner. There's no house for a lien to sit against quietly for years — IRS enforcement reaches you directly, through your paycheck and your bank account. A wage levy is continuous until released, and a bank levy freezes funds for 21 days before they're sent to the Treasury. None of that is happening today, and none of it has to happen at all — but the pipeline runs on automation, and automation never forgets a balance.

| Notice | Your window | What's lost if it passes |

|---|---|---|

| CP23 | The "pay by" date printed on the notice | The cheapest exit — the balance keeps compounding and reminders begin |

| CP501 / CP503 | The date printed on each reminder | No formal right yet, but the account moves steadily toward enforcement |

| CP504 | The date printed on the notice | Your state tax refund becomes seizable, and a federal tax lien becomes likely |

| LT11 / Letter 1058 | 30 days from the notice date | Your pre-levy Collection Due Process hearing (Form 12153) — after that, wage and bank levies are legal |

Holding a CP23 you don't understand?

Send us a photo of it before the payment date printed on it passes. An experienced tax professional will trace the payment mismatch, tell you whether the IRS or your return is right, and map your options — free, confidential, no pressure.

Your options if the CP23 balance is correct

A correct CP23 balance qualifies for every standard IRS resolution program — the notice only advertises "pay in full," but the real menu is longer. Which option fits depends on the size of the balance and what your budget can actually absorb:

| Option | Best for | Upfront cost | Timeline |

|---|---|---|---|

| Pay in full | You have the cash and the balance is right | None | Immediate — stops penalties and the notice sequence |

| Short-term payment plan | You can clear the balance within 180 days | $0 setup | Up to 180 days; interest and penalty continue |

| Long-term installment agreement | Balances of $50,000 or less | Setup fee (lower with direct debit; reduced for low income) | Up to 72 months, set up online |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living costs | $0 | Collection paused; the debt remains and interest accrues |

| Offer in Compromise | Your assets and income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Months of review; roughly 1 in 5 offers accepted in FY2024 |

| Penalty abatement | Clean compliance for the prior 3 years, or reasonable cause | $0 | Removes penalties, not tax; automatic relief (AEP) begins summer 2026 |

Two CP23-specific notes on that menu. First, if this is your first slip after years of clean filing, first time penalty abatement can strip the failure-to-pay penalty from the balance — and starting summer 2026, the IRS's new Automatic Exemption from Penalty applies similar relief without a request. Second, a CP23 sometimes includes a separate estimated-tax underpayment charge on top of the missing-payment balance; that penalty arrives on its own notice — see our CP30 notice guide — and has its own waiver rules.

Whatever you choose, know what waiting costs: you can estimate how fast your specific balance grows with our IRS penalty and interest calculator. For setup mechanics, our walkthrough on how to set up an IRS payment plan online covers the whole process screen by screen.

A worked example: tracing a $31,200 CP23

Say you're self-employed, you rent your apartment, and your CP23 says you owe $31,200. Here's how the math typically breaks down — and how differently the two paths end. (This is a hypothetical illustration, not a client case.)

Your return claimed four quarterly payments of $9,500 — $38,000 total. The IRS's records show only one $9,500 payment posted. The gap is $29,000 minus a small credit adjustment — call it $28,500 in tax — plus roughly $2,700 in failure-to-pay penalty and accrued interest, landing at the $31,200 printed on the notice.

Path one: the payments exist but posted wrong. You pull your bank records and find Q2 and Q3 ($19,000) were paid from your spouse's IRS Direct Pay profile under her SSN, and your Q4 payment ($9,500), made in January, defaulted to the new tax year. You call the notice number with all three confirmation numbers and request transfers. When the payments move, the $28,500 tax gap closes and, because the payments were made by their due dates, the $2,700 in penalty and interest is recomputed off with them — if a payment actually posted late, part of that accrual survives the correction. Your out-of-pocket cost: an hour on the phone.

Path two: you actually skipped the quarters. The money never left your account — cash-flow crunches ate Q2 through Q4. At $31,200 you're under the $50,000 threshold, so a streamlined installment agreement can be set up online: $31,200 ÷ 72 months ≈ $433/month, though interest and the 0.5% monthly penalty keep accruing on the shrinking balance, so paying more than the minimum always costs less in total. As a renter, this plan is also what stands between you and the wage or bank levy the later notices authorize — an active agreement stops the escalation sequence cold.

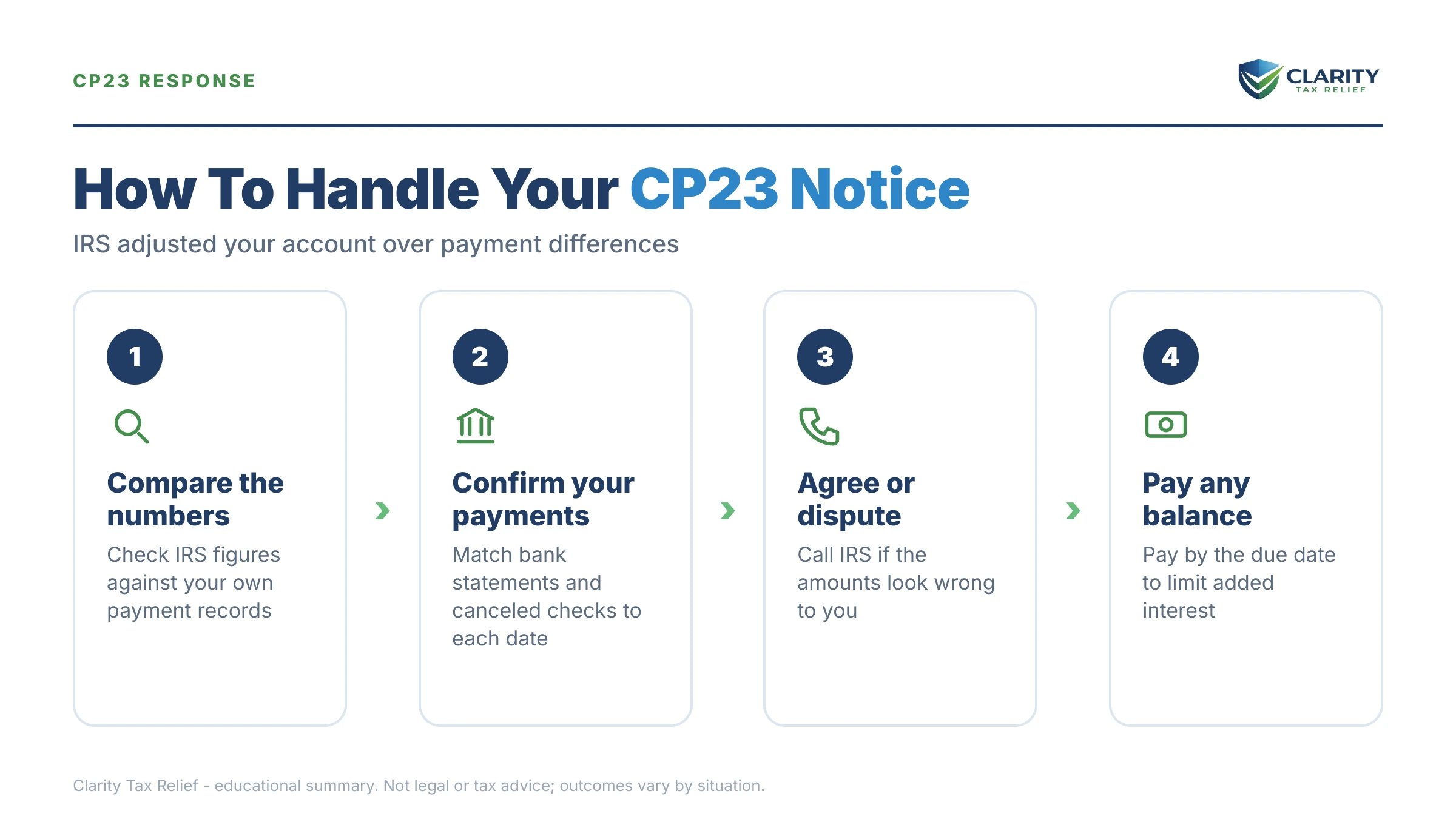

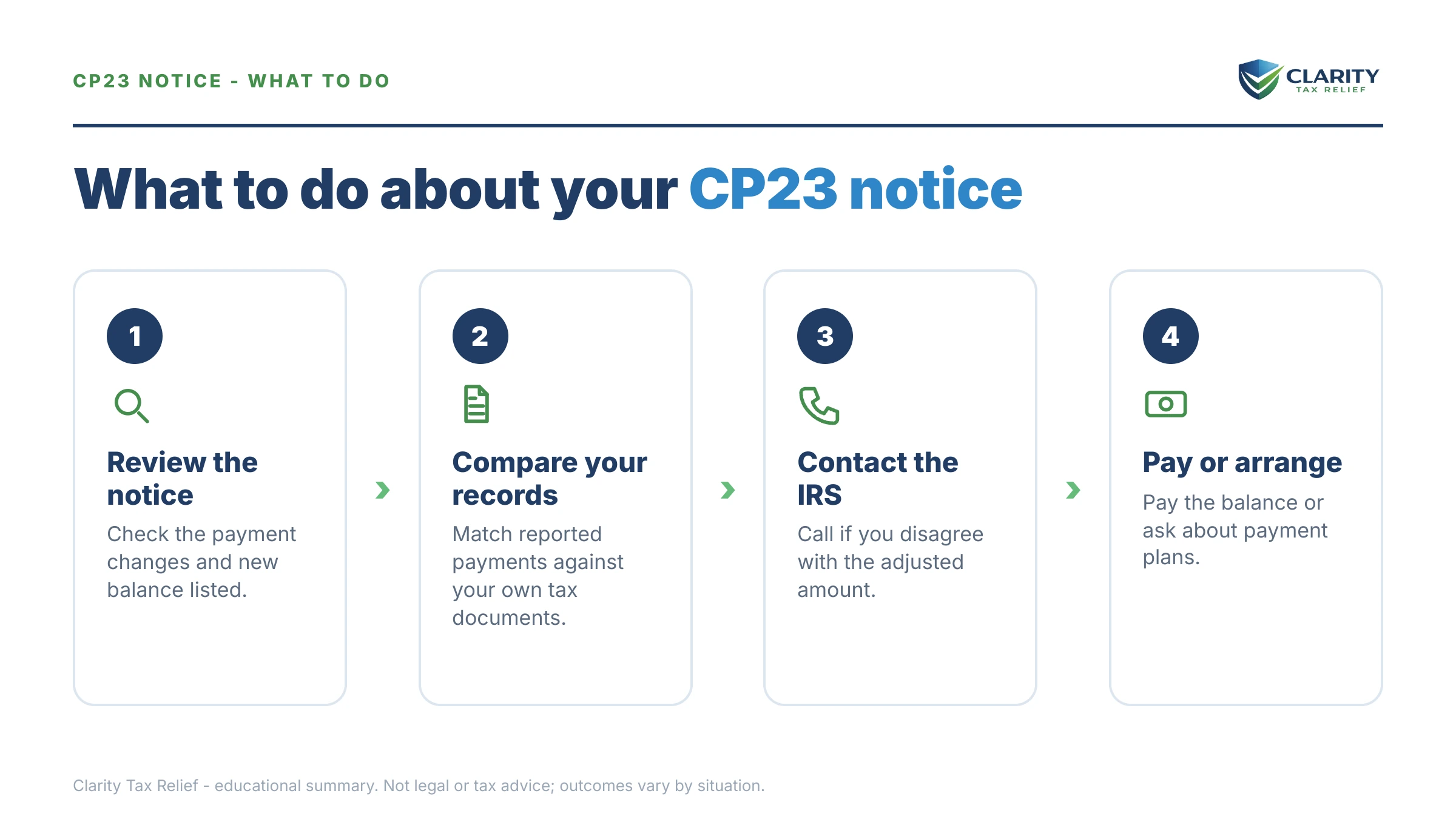

How to respond to a CP23 notice, step by step

- Pull the IRS's payment record. Log into your IRS online account or request an account transcript, and list every estimated payment the IRS shows posted for the tax year — with dates and amounts.

- Match each payment to your own proof. Gather Direct Pay or EFTPS confirmations, canceled checks, and bank statements, and identify the exact payment the IRS is missing.

- Dispute a misapplied payment fast. Call the number printed on the top right of your CP23 or respond in writing with copies of your proof, and ask the IRS to move any payment posted to the wrong year or Social Security number.

- Pay or arrange a plan if the balance is real. Pay by the notice date at IRS.gov/payments, or set up a short-term plan or installment agreement before that date passes.

- Fix the cause for next year. Confirm every future quarterly payment posts to the right tax year and the right SSN within a week of paying it.

That last step matters more than it sounds. A CP23 almost always reveals a process problem — payments made from the wrong account, or January payments that default to the wrong year. If quarterlies are new territory for you, our primer on how do quarterly estimated taxes work shows how to pay so the credit lands where you expect it.

CP23 vs. CP24 vs. CP25 — and the math-error cousins

The CP23 is one of three notices the IRS sends for the same estimated-payment mismatch; only the balance outcome differs. If the correction still leaves you a refund, you get a CP24 notice. If it zeroes out — no refund, no balance — you get a CP25 notice. Only the CP23 starts a collection clock.

Don't confuse these with the math-error notices: a CP11 notice means the IRS corrected a calculation error and you owe, and a CP12 notice means a correction changed your refund. Those involve the return's arithmetic; your CP23 is strictly about payments that did or didn't reach your account.

When you can handle a CP23 yourself

Plenty of CP23s never need professional help. If your account transcript shows the payment posted to the wrong year and you have the confirmation number, one phone call usually fixes it. If the balance is real, small, and you can pay it within 180 days, the short-term plan is free to set up and takes minutes online. If the mismatch was your own typo and you can afford the corrected amount, just pay it by the notice date and move on.

Experienced help changes outcomes in a narrower set of situations: the mismatch spans multiple years or involves a divorce-year split of joint estimated payments; you've already let the sequence run to a CP504 or LT11 and a levy is in motion; the balance is large and you need the sequencing of penalty relief, payment transfers, and a payment plan done in the right order; or you also have unfiled returns that will surface the moment you call the IRS. In those cases, the order of operations — not just the answer — determines what you pay. A free review with an experienced tax professional can tell you which camp you're in before you spend anything: request one here or call (888) 825-7779.

Terms on your CP23, decoded

- Estimated tax payments — the quarterly prepayments (Form 1040-ES) that people without withholding make toward the year's tax; the credits your CP23 says don't match.

- Adjustment — the IRS's correction to your return's payment line; it changes your balance without an audit.

- Account transcript — the IRS's line-by-line record of your tax year, including every payment it posted; your best evidence in a CP23 dispute.

- Failure-to-pay penalty — 0.5% of the unpaid tax per month, running from the return's due date until the balance is paid or the payment mismatch is corrected.

- Estimated tax penalty — a separate charge for paying quarterlies late or short during the year; it can survive even after a misapplied payment is fixed, depending on when the payment was actually made.

- Levy — the IRS's power to take wages, bank funds, or other property; it exists only at the end of the notice sequence, never at the CP23 stage.

CP23 notice questions, answered

What is a CP23 notice from the IRS?

A CP23 notice means the IRS adjusted your return because the estimated tax payments you claimed don't match the payments posted to your account, leaving a balance due. It usually traces back to a payment applied to the wrong year or the wrong Social Security number rather than a payment you never made. Check the payment records in your IRS online account before you pay anything.

Why don't my estimated tax payments match IRS records?

The most common reasons are a payment applied to the wrong tax year, a payment made under your spouse's SSN that never reached the joint return, a prior-year overpayment you expected to carry forward that was reduced or offset, or a typo on your return. Your IRS account transcript lists every payment that actually posted, with dates and amounts, so you can spot exactly which quarter is missing.

What should I do if I disagree with my CP23 notice?

Contact the IRS at the number printed on the top right of your notice, or respond in writing, with proof of every payment: Direct Pay or EFTPS confirmations, canceled checks (front and back), or bank statements. Your CP23 states its own dispute window, so act before that date passes. If a payment posted to the wrong year or SSN, ask the IRS to move it — the related penalty and interest come off once the correction posts.

Do I have to pay a CP23 while I'm disputing it?

You aren't required to pay a disputed balance immediately, but interest and the 0.5% monthly failure-to-pay penalty keep accruing until the account is corrected or paid. If the dispute may take months and the amount is large, some taxpayers pay first and recover the money once the record is fixed. When you have clear proof the payment was made, most disputes end with a corrected account rather than out-of-pocket cash.

Is a CP23 notice an audit?

No. A CP23 is an account adjustment, not an examination — the IRS isn't questioning your income or deductions, only reconciling the payments you claimed against the payments it received. No auditor is assigned and no receipts are requested. If the balance turns out to be real, it's handled like any other tax bill, with the same payment options.

What's the difference between CP23, CP24, and CP25?

All three report the same problem — the estimated tax payments on your return don't match IRS records — but with different outcomes. A CP23 means the change leaves you owing money, a CP24 means you're still due a refund, and a CP25 means the change zeroes out with no refund and no balance. Only the CP23 starts a collection clock, which is why it deserves the fastest response of the three.

Can I set up a payment plan for a CP23 balance?

Yes. A CP23 balance qualifies for the same IRS payment plans as any other tax debt: up to 180 days with no setup fee on a short-term plan, or a monthly installment agreement — balances of $50,000 or less can generally be set up online for up to 72 months. Interest and the failure-to-pay penalty keep running while you pay, so a larger monthly payment always costs less overall.

Can the IRS levy my bank account over a CP23?

Not immediately — a CP23 carries no levy power by itself. But an unpaid CP23 balance feeds the automated collection sequence: reminder notices, then a CP504 that lets the IRS seize your state tax refund, then an LT11 final notice that starts a 30-day clock before wage and bank levies become legal. Every one of those steps is avoidable by paying, arranging a plan, or resolving the dispute now.

Your next 24 hours

- Find two things on your CP23: the "pay by" date, and the side-by-side payment comparison showing what you claimed versus what the IRS posted. That comparison is the entire case.

- Gather your proof: your filed return, the notice, and every quarterly payment record — Direct Pay or EFTPS confirmations, canceled checks, and the bank statements they cleared through.

- Get a free case review before the notice date passes: use the 2-minute form or call (888) 825-7779, and an experienced tax professional will trace the mismatch and tell you whether to dispute, pay, or set up a plan.

Official references: the IRS's own explainer at Understanding your CP23 notice, payment options at IRS.gov/payments, and plan details at the IRS payment plans page.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.