State Back Taxes

Virginia Back Taxes in 2026: What Virginia Tax Can Do — and How to Resolve It

The short answer: Virginia back taxes are collected by Virginia Tax (the Virginia Department of Taxation), which can freeze bank accounts, garnish wages, and record a lien with judgment force — all without suing you first. Pay by the due date on your bill, or set up a payment plan at tax.virginia.gov before enforcement starts.

The letter on your kitchen table isn't from the IRS — it's from the Commonwealth, and if you earn on 1099s, you already know how it happened: the money came in with nothing withheld, May 1 came and went, and now the balance printed on the bill is bigger than the tax you actually skipped. Here's what matters: Virginia Tax follows a predictable script, and every stage of that script has an exit — the earlier you take one, the cheaper it is.

If you're not sure which notice you're even holding, the image below shows exactly what a Virginia Tax bill looks like and where to find the assessment date, the account number, and the due date that starts your clock.

⏱ Your deadlines: the due date printed on your Notice of Assessment — typically about 30 days from the bill date — is when Virginia expects payment or an arrangement. If you dispute the amount, Virginia's administrative appeal window is generally 90 days from the assessment date. Miss both and the account moves to Collections while penalties and interest keep running.

Why you owe Virginia back taxes

The Virginia Department of Taxation bills a balance for one of four reasons: you filed without paying, you never filed, the IRS changed your federal return, or you missed the estimated payments Virginia expects from 1099 earners. Which one applies to you changes the fix, so pin it down first.

You're self-employed and nothing was withheld. Virginia expects quarterly estimated payments from contractors — the vouchers run on the state's own calendar (May 1, June 15, September 15, and January 15), not the federal one. Skip them and the whole year's tax lands at once, with an underpayment addition on top. If that's your pattern every year, fix the plumbing with our guide to how quarterly estimated taxes work — and remember the federal side of the same income carries its own self-employment tax hit.

The IRS adjusted your federal return. Virginia's return starts from your federal numbers. When a CP2000 notice or an audit raises your federal income, Virginia gets the data and issues its own assessment for the state share — often a year or more later, when you thought the problem was closed. You're also required to report federal changes to Virginia yourself; waiting for the state to find them just adds penalty months.

You never filed a Form 760. Virginia receives IRS income data and can assess tax without a return from you — using your gross income and none of your deductions. Those estimated assessments are almost always higher than what a real return would show, which is why filing late still usually shrinks the bill.

The May 1 trap. Virginia's individual filing deadline is May 1, not April 15, and the state grants an automatic six-month filing extension with no form required. But that extension is time to file, not time to pay — pay too little by May 1 and an extension penalty of roughly 2% per month starts stacking before the bigger late-payment penalty even enters the picture.

What happens if you ignore Virginia back taxes

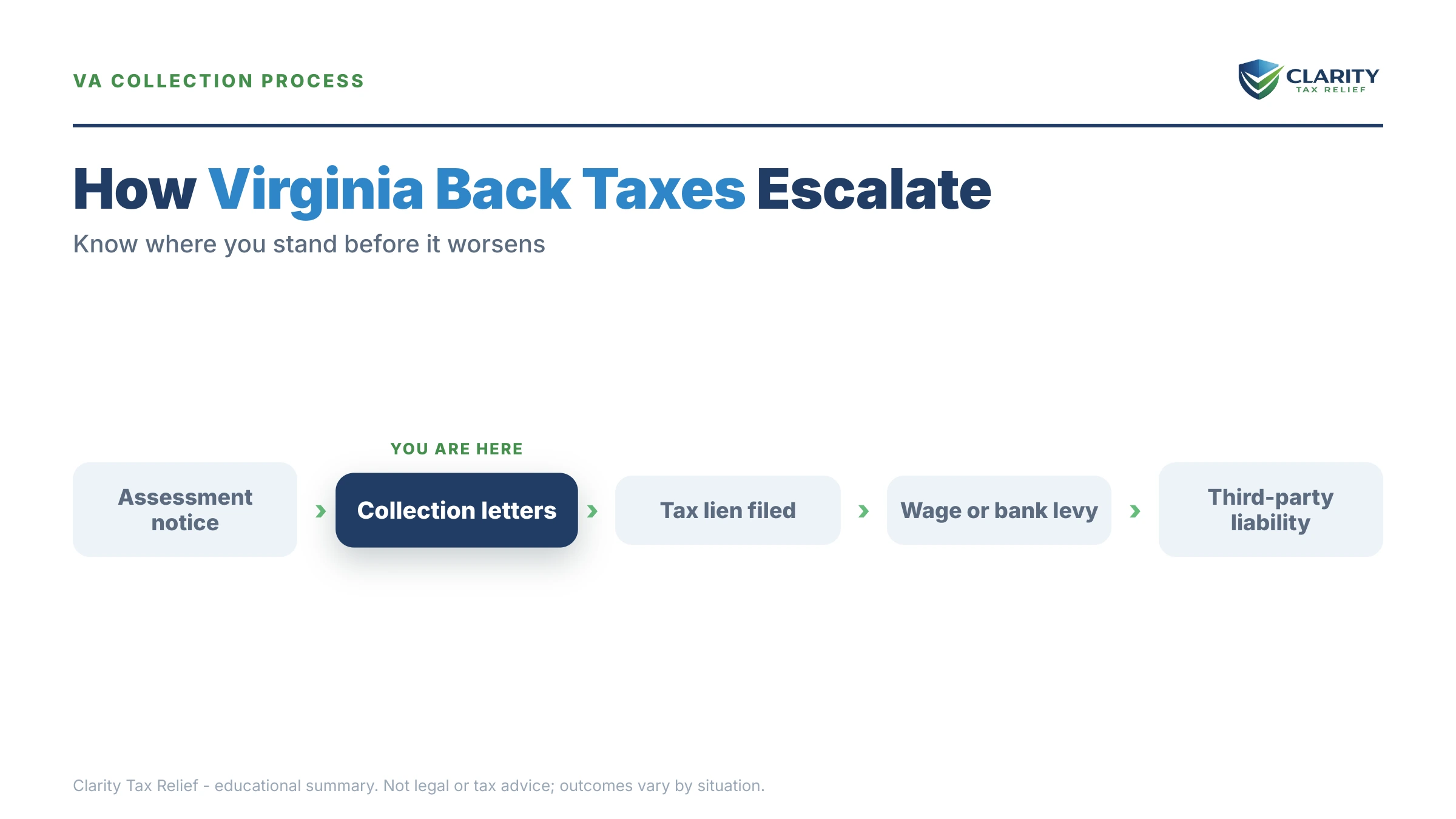

Virginia Tax can freeze your bank account and garnish your pay without ever taking you to court — its liens are administrative, issued directly by the collections system. The sequence below is largely automated, and each stage is harder to unwind than the one before it:

- Notice of Assessment. The bill. It shows the tax year, the balance, and a due date — typically about 30 days out. No enforcement yet; this is the cheapest moment you will ever have.

- Collection notices. Past-due letters follow, the account moves to Virginia Tax's collections operation, and the 6%-per-month late-payment penalty keeps compounding toward its 30% cap.

- Refund offsets. Any Virginia refund you're owed is applied to the debt automatically, and the state can intercept your federal refund through the Treasury Offset Program.

- Third-party liens. Virginia issues a bank lien to your bank — which must hold and remit your funds — or a wage lien to your employer or, for contractors, to businesses that pay you. No court hearing comes first.

- Memorandum of lien. Virginia records a lien with the circuit court that carries the force of a judgment: public record, attached to your real estate, and a roadblock to any refinance or clean sale until satisfied.

- Business-level enforcement. For unpaid trust taxes like sales tax or employee withholding, Virginia can revoke registrations, padlock a business, and issue a converted assessment that makes responsible individuals personally liable.

One 2026 reality check: while IRS enforcement has been slowed by staffing cuts, state collection systems like Virginia's never depended on that workforce. The state's automation keeps issuing liens on schedule — the quiet mailbox is not a truce.

| Document or action | The window | What's at stake |

|---|---|---|

| Notice of Assessment (the bill) | Due date printed on the bill — typically about 30 days | Pay or arrange payment before the account moves to Collections |

| Administrative appeal to the Tax Commissioner | Generally 90 days from the assessment date | Your main route to dispute the tax without paying it first |

| Wage lien or bank lien issued | Act immediately — the money is already claimed | A payment arrangement is usually the fastest release path |

| Memorandum of lien recorded in circuit court | Already public record | Blocks a clean refinance or sale of Virginia real estate until resolved |

| Padlocking / converted assessment (business trust taxes) | After repeated non-payment of sales or withholding tax | The business can be closed and owners or officers assessed personally |

Holding a Virginia Tax bill right now?

Virginia's 6%-per-month late-payment penalty is already running, and its liens arrive without a court hearing. Get your Virginia assessment reviewed free before the due date on your bill passes — an experienced tax professional will map exactly where your account sits and which option costs you least.

Your options for resolving Virginia back taxes

Most Virginia back-tax balances are resolved one of four ways: full payment, a payment plan, a penalty waiver, or — in genuinely limited finances — an Offer in Compromise. Virginia's programs are real but leaner than the IRS's, and eligibility is means-tested, not marketed.

| Option | Who it fits | Cost and catch |

|---|---|---|

| Pay in full | Anyone who can raise the money — the penalty stack stops growing the day the balance hits zero | Nothing but the balance; ask about a penalty waiver even after paying |

| Virginia payment plan | Most individuals with filed returns; set up through Individual Online Services or by phone | Interest (federal underpayment rate + 2%) continues; a missed payment can restart liens |

| Penalty waiver for reasonable cause | Illness, disaster, or reliance on bad advice behind the late filing or payment | Written request with proof; Virginia has no automatic first-time pass, and interest is rarely removed |

| Offer in Compromise — doubtful collectibility | Taxpayers whose income and assets genuinely cannot cover the balance | Full financial disclosure; discretionary approval by the Tax Commissioner — never guaranteed |

| Offer in Compromise — doubtful liability | You have a real argument you don't owe the assessed tax | Requires documentation of the dispute; often paired with (or replaced by) the 90-day appeal |

| Administrative appeal | The assessment is wrong — wrong year, wrong income, residency error, missed credits | Generally must be filed within 90 days of assessment; collection on the disputed amount can pause while it's decided |

| Hardship pause | Paying anything would leave you unable to cover basic living expenses | Virginia has no formal published hardship program like IRS CNC status — pauses are negotiated case-by-case with financial proof, and the debt keeps growing |

Two options that don't exist in 2026 deserve a flag. First, Virginia's last tax amnesty ran in 2017; there is no standing amnesty, so anyone promising one is selling something. Second, Virginia has no equivalent of the IRS's first-time penalty abatement — every state waiver request has to stand on reasonable cause, in writing, with documentation.

If unfiled years are part of your picture, they come first: Virginia won't finalize a plan or consider an offer while required returns are missing. Lost your records? Our guide to filing back taxes without records walks through rebuilding income figures from IRS wage transcripts — which work for your Form 760 too, since Virginia starts from federal numbers.

What a $36,900 back-tax balance looks like for a Virginia contractor

Say you're a 1099 IT contractor in Chesterfield County who skipped quarterlies for 2023 through 2025. Your combined balance is $36,900 — roughly $30,200 federal and $6,700 Virginia — and the two pieces grew at very different speeds. This example is hypothetical, but the arithmetic is how both systems actually work.

The Virginia side started as about $4,900 in unpaid tax. The late-payment penalty accrued at 6% per month and hit its 30% cap in just five months: $4,900 × 30% = $1,470. Interest at the federal underpayment rate plus 2% added roughly another $330 over the unpaid stretch. Total: about $6,700 — nearly 37% growth on the original tax, most of it in the first half-year.

The federal side grew slower per month (failure-to-pay runs 0.5% monthly) but compounds over years — you can rough out your own federal accruals with our IRS penalty & interest calculator.

Now the resolution math. On the Virginia $6,700, a two-year payment plan runs about $6,700 ÷ 24 ≈ $280/month plus ongoing interest. On the federal $30,200 — under the $50,000 streamlined ceiling — a 72-month online agreement starts around $30,200 ÷ 72 ≈ $420/month before accruals; setting up the IRS payment plan online takes minutes once your returns are filed. Notice the strategy hiding in those numbers: because Virginia's rates are higher and its liens move faster, retiring the state balance on the shorter clock while stretching the federal one is usually the cheaper sequencing — the full decision framework is in our guide to state tax debt vs. IRS: which to resolve first.

Virginia Tax vs. the IRS: why the state bill grows faster

Virginia's late-payment penalty accrues at 6% per month — twelve times the IRS rate of 0.5% — and caps at 30% instead of 25%. If you owe both agencies, understanding the differences below is what keeps you from applying federal assumptions to a state problem.

| Item | Virginia Tax | IRS |

|---|---|---|

| Individual filing deadline | May 1 | April 15 |

| Late-filing penalty | 6% per month, up to 30% | 5% per month, up to 25% |

| Late-payment penalty | 6% per month, up to 30% (cap reached in 5 months) | 0.5% per month, up to 25% |

| Interest rate | Federal underpayment rate + 2 points — always above the IRS rate | Federal underpayment rate |

| First-time penalty relief | None — reasonable cause only | First-Time Abate, being replaced by the Automatic Exemption from Penalty (AEP) starting summer 2026 |

| Wage garnishment | Administrative wage lien — no court order, limited advance warning | Levy only after a final notice (LT11/Letter 1058) and a 30-day appeal window |

| Lien on property | Memorandum of lien recorded in circuit court, with judgment force | Notice of Federal Tax Lien |

| Collection timeline | State-specific rules — not the federal 10-year statute; recorded liens have a long enforcement life | 10 years from assessment (the CSED), subject to tolling |

The pattern to take away: the IRS gives more warning; Virginia charges more per month. Federal collection is a long staircase of notices with formal appeal rights at the top — mapped in our complete IRS collection roadmap. Virginia's staircase is shorter and its liens land earlier.

How to resolve Virginia back taxes, step by step

- Confirm what Virginia says you owe. Log in to (or create) an Individual Online Services account at tax.virginia.gov, or call Virginia Tax, and list every year on the account with its tax, penalty, and interest.

- File any missing Virginia returns. File every unfiled Form 760, even years late — real returns usually beat the state's estimated assessments, and they're required before any plan or offer will be considered.

- Pick your resolution before the due date on your bill. Pay in full if you can; otherwise set up a payment plan online or start an offer or waiver request — any arrangement on record beats silent default.

- Request a penalty waiver in writing if you have reasonable cause. Serious illness, disaster, or reliance on bad professional advice can support removing some or all of Virginia's penalty stack — ask; the interest stays either way.

- Coordinate the federal side. If the same missed income created an IRS balance, set up the federal resolution too, so one agency's refund offset doesn't blow up the other agency's plan.

- Get experienced help if a lien is already in motion. A wage lien, bank lien, or recorded memorandum of lien changes the order of operations — have an experienced tax professional negotiate the release while the resolution is built.

When you can handle Virginia back taxes yourself

Plenty of Virginia balances don't need professional help — and knowing which kind you have is worth more than any sales pitch. Handle it yourself when it's one tax year, you agree with the numbers, and you can pay within a few months: log in, set up the plan online, request a reasonable-cause waiver if you honestly have one, and move on. The same is true for a bill you can simply pay — pay it, then dispute penalties afterward if warranted.

Experienced help changes the outcome in a different set of situations: a wage or bank lien already issued (release negotiations are time-critical and evidence-driven); a memorandum of lien blocking a home sale or refinance; multiple unfiled years with both Virginia and the IRS billing you at once, where the sequence of filings and plans determines what you pay; an Offer in Compromise, where the financial-disclosure math decides everything; a residency or federal-adjustment dispute inside the 90-day appeal window; or any business trust-tax case where a converted assessment could reach you personally. In those cases the fee for representation is usually competing against a much larger enforcement cost.

If your situation sits on that second list — a lien already recorded, two agencies billing you at once — a free case review or a call to (888) 825-7779 will map the order of operations before you commit to anything.

Terms on your Virginia notices, decoded

- Notice of Assessment — Virginia's official bill: the state has formally recorded that you owe a specific amount for a specific year, and the appeal and payment clocks run from its date.

- Memorandum of lien — a lien Virginia records with the circuit court that carries the force of a judgment, attaching to your real estate and appearing in title searches.

- Third-party lien — Virginia's administrative order to someone who holds your money (your bank, employer, or a business that pays you) to send it to the state instead.

- Converted assessment — Virginia's tool for making owners, officers, or other responsible people personally liable for a business's unpaid trust taxes like sales tax or withholding.

- Debt setoff — the automatic capture of your state or federal refund to pay a Virginia balance, including through the federal Treasury Offset Program.

- Padlocking — Virginia's authority to physically close a business that keeps operating without paying its trust taxes.

Virginia back taxes: your questions, answered

How long can Virginia collect back taxes?

Longer than most people hope — and Virginia's timeline is not the IRS's 10-year rule, so don't apply federal math to a state bill. Once Virginia records a memorandum of lien in circuit court, that lien has a long enforcement life against your property and income. Waiting out the clock is not a realistic strategy for a Virginia balance; resolving it is.

Can Virginia Tax garnish my wages without a court order?

Yes. Virginia Tax issues third-party liens — wage liens sent to your employer and bank liens sent to your bank — administratively, without suing you first. Your employer is legally required to comply, and Virginia's withholding rules differ from the federal garnishment limits many people expect. The fastest release path is usually a payment arrangement made directly with Virginia Tax collections.

Does Virginia have a payment plan for back taxes?

Yes. Most individuals can set up a payment plan through an Individual Online Services account at tax.virginia.gov or by calling Virginia Tax collections. Interest — the federal underpayment rate plus 2% — keeps accruing until the balance is paid, and a missed payment can put liens back in play, so choose a monthly amount you can actually sustain.

Does Virginia have an Offer in Compromise?

Yes, but it's narrower than the IRS version. Virginia accepts offers based on doubtful collectibility — your finances show you genuinely cannot pay in full — or doubtful liability, where you dispute that you owe the tax at all. Approval is discretionary, requires full financial disclosure, and is far from automatic, so have the math checked before you file.

Will Virginia take my federal tax refund?

It can. Virginia participates in the Treasury Offset Program, which lets the state intercept your federal refund for unpaid Virginia taxes. It works the other way too: the IRS can take your Virginia refund through the State Income Tax Levy Program. If you owe both agencies, expect every refund to be intercepted until both balances are resolved.

What is a memorandum of lien in Virginia?

A memorandum of lien is Virginia Tax's version of a recorded tax lien: it is filed with the circuit court and carries the force of a judgment against you. It attaches to your real estate, becomes a public record that lenders find in title searches, and will block a clean sale or refinance until it is satisfied. Paying or resolving the underlying balance is what gets it released.

What happens if I never filed my Virginia returns?

Virginia will eventually fill in the numbers for you — the state receives your federal data from the IRS and can assess tax based on it, usually without the deductions a real return would claim. That assessment is collectible just like a filed balance. Filing the actual Form 760s, even years late, typically lowers the bill and is the required first step before any payment plan or offer.

Are Virginia's penalties worse than the IRS's?

For late payment, dramatically. Virginia's late-payment penalty runs 6% per month up to a 30% cap — twelve times the IRS's 0.5% monthly rate — and it hits that cap in just five months. Virginia also charges interest at the federal underpayment rate plus 2%, so the same balance grows faster in Richmond's system than in the IRS's.

Should I pay Virginia or the IRS first if I owe both?

Usually you resolve both at once — but Virginia often deserves the faster payoff. Its penalty and interest rates are higher, and its wage and bank liens arrive with less warning than IRS levies. The IRS offers longer, more flexible payment plans, so stretching the federal balance while retiring the state one is a common strategy. See our guide to state tax debt vs. IRS for the full framework.

Your next 24 hours

- Find three things on your Virginia bill: the assessment date (it starts the 90-day appeal clock), the due date, and your account number — you'll need all three for any call or online setup.

- Gather your paper: your last filed federal return and Form 760, every Virginia notice you've received, and this year's income records (1099s, bank deposits) so the missing years can be reconstructed.

- Get the free case review — the two-minute form or (888) 825-7779. Virginia's 6%-per-month penalty and above-federal interest are accruing while the bill sits in the drawer; an experienced tax professional can tell you in one call whether a plan, waiver, appeal, or offer fits your numbers.

Primary sources for this guide: the Virginia Department of Taxation (bills, payment plans, offers, and appeals all run through tax.virginia.gov), the IRS payment plans page for the federal side of a combined balance, and the Taxpayer Advocate Service for federal hardship situations.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.