IRS Notices

IRS CP215 Notice: Business Civil Penalty Explained (2025)

The short answer: a CP215 notice is the IRS telling your business it has assessed a civil penalty. The penalty — printed on the notice with the form, period, and reason — is already on your business account. You generally have until the "pay by" date (often about 21 days) to pay, dispute it, or request that it be removed.

Holding a CP215 right now?

Send us a photo of it. An experienced tax professional will decode exactly why the penalty was assessed and whether your business may qualify to have it removed — free, confidential, no pressure.

⏱ Your deadline: the "pay by" date printed on the notice — typically 21 days from the notice date. After that, interest keeps accruing and the balance moves into the IRS business collection sequence. You can still dispute the penalty or request relief after the date, but acting early keeps the most options open.

Why your business got a CP215

A CP215 is a "civil penalty notice." It means the IRS reviewed a business filing — or the lack of one — and decided a penalty applies. Unlike a regular tax bill, this isn't tax you reported and didn't pay. It's a penalty the IRS added on its own. The notice spells out the form, the tax period, the dollar amount, and the Internal Revenue Code section behind it (the IRS's overview is at Understanding your CP215 notice).

The most common triggers are:

- Late or unfiled employment-tax returns — Form 941 (quarterly payroll) or Form 940 (federal unemployment) filed after the deadline.

- Missed payroll-tax deposits — deposits made late, in the wrong amount, or through the wrong method.

- Information-return problems — W-2s, 1099s, or similar forms filed late, not filed, or filed with missing or incorrect information.

- Other return-filing penalties — including partnership or corporate filings submitted after their due date.

Read the reason line carefully. The penalty type controls which relief options are open to you and what proof you'll need.

What happens if you ignore it

A CP215 balance doesn't disappear, and the business collection system is automated. Ignore it and the sequence keeps moving — each step adding interest and enforcement power:

- CP215 — the penalty is assessed. You are here. No enforcement yet.

- Reminder notices — balance-due statements as interest keeps growing on the unpaid penalty.

- Notice of Intent to Levy — the IRS warns it can seize business funds and may file a federal tax lien against business assets.

- Final Notice & levy — after the final notice and a 30-day window, the IRS can levy business bank accounts and accounts receivable. You have appeal rights here, but fewer good options than today.

If the penalty relates to unpaid payroll taxes, there's a second risk most owners don't see coming: the Trust Fund Recovery Penalty can be assessed personally against owners and other responsible people. That's a separate process — but a CP215 about employment taxes is a signal to take the whole payroll picture seriously.

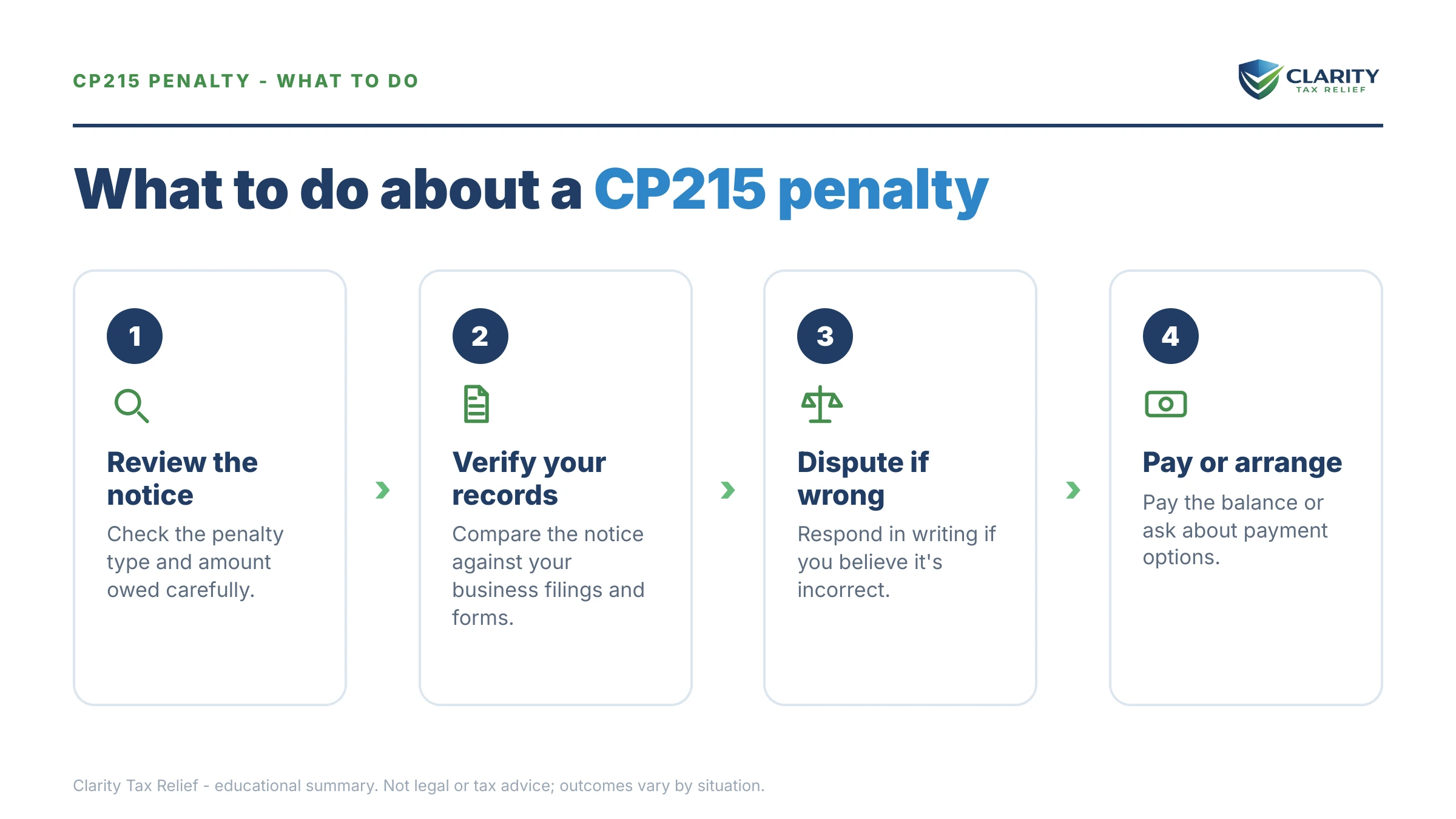

First: make sure the CP215 is actually right

Civil penalty notices are sometimes wrong or based on outdated information. Before you pay, take a few minutes to confirm the facts:

- Match the form and period. Does the notice point to a return you actually filed late? Was it really late, or did the IRS post your filing or deposit to the wrong period?

- Check your records and deposits. Pull the filing confirmation and your payroll-deposit history. A deposit applied to the wrong quarter can generate a penalty that isn't truly owed.

- Screen for scams. A real CP215 arrives by postal mail, never email or text. Real IRS payments go only to the United States Treasury or through IRS.gov — anyone demanding gift cards, wire transfers, or payment apps is a criminal, not the IRS.

If the notice is wrong, respond in writing with documentation — proof of timely filing, corrected figures, or deposit records. Don't pay a penalty your business doesn't owe on the hope the IRS will fix it later.

How to get the penalty removed or reduced

Even when the facts are correct, a CP215 penalty can often be removed or lowered. Which path fits depends on your business's history and what caused the problem:

- First-time penalty abatement. If your business filed and paid on time for the past three years, first-time penalty abatement can wipe out the penalty entirely — often with a single phone call or letter.

- Reasonable-cause relief. If the penalty came from something outside your control — serious illness, a natural disaster, records lost in a fire, or reliance on incorrect professional advice — reasonable-cause relief may apply. You'll need to explain what happened and back it up.

- Dispute the assessment. If the IRS's facts are wrong, you can challenge the penalty itself rather than ask for forgiveness. Send proof and ask the IRS to reverse it.

- Set up a payment plan. If the penalty is correct and your business can't pay all at once, an installment agreement (see the IRS payment plans page) keeps enforcement off while you pay it down.

It helps to understand the difference between the failure-to-file and failure-to-pay penalties, because the relief request and the proof you need are not the same for each.

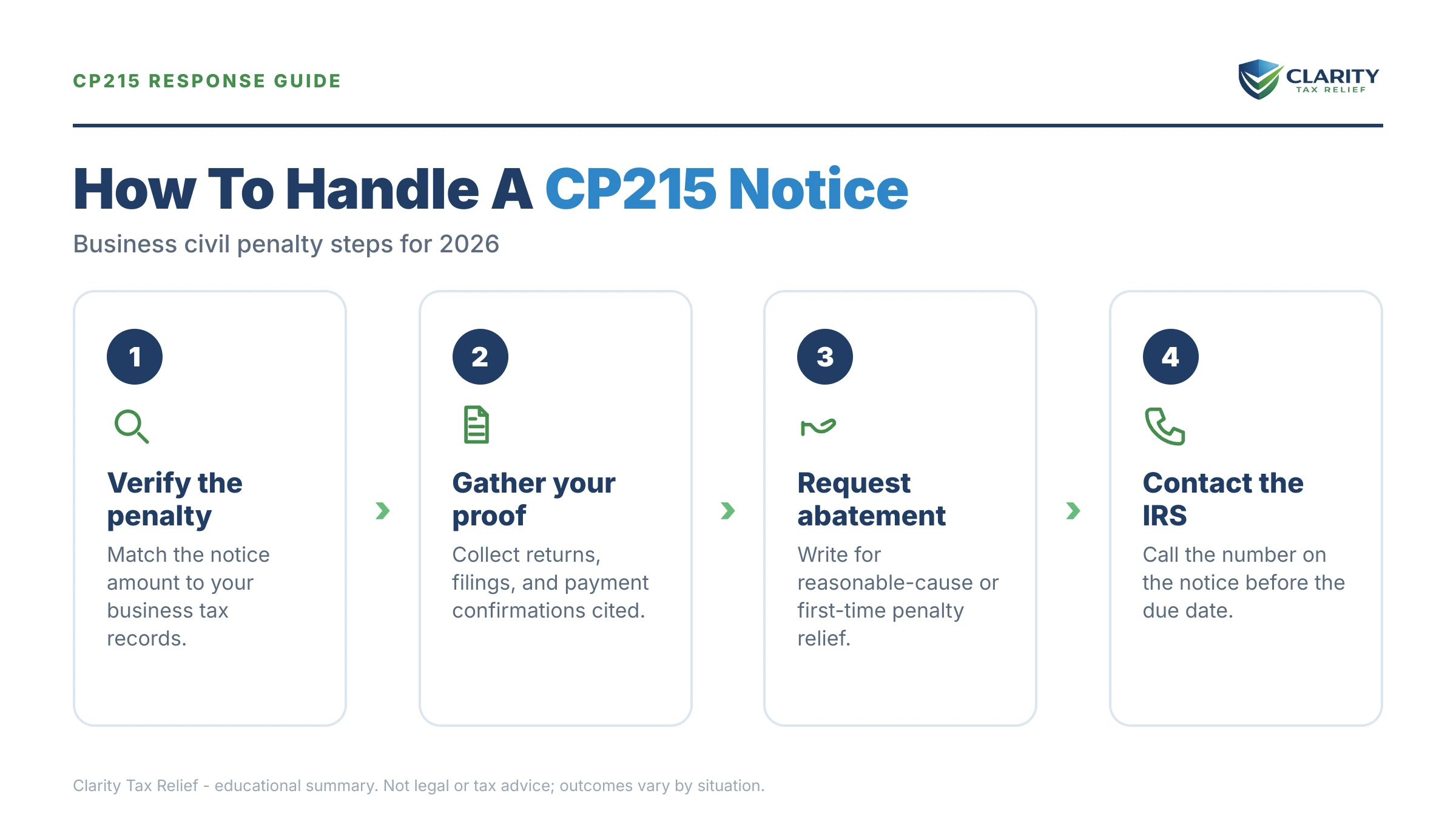

How to respond, step by step

- Verify the penalty. Match the form, period, and reason against your filing and deposit records.

- If the notice is wrong: respond in writing with proof — keep copies of everything you send and how you sent it.

- If it's correct and you may qualify for relief: request first-time abatement or reasonable cause before the pay-by date.

- If it's correct and you can pay: pay by the deadline at IRS.gov/payments to stop interest and the collection sequence.

- If it's correct but you can't pay in full: set up an installment agreement before the deadline so enforcement doesn't begin.

- If the penalty involves payroll taxes or unfiled employment returns: get a professional review — the order you fix things in (file returns, then address penalties, then the balance) changes what you ultimately pay, and personal exposure may be in play. See our guide to 941 back taxes for a business.

CP215 questions, answered

What is a CP215 notice?

A CP215 is the IRS notice that assesses a civil penalty against a business. It tells you the penalty has already been charged to your business account, the dollar amount, the tax form or period it relates to, and the reason — often a late or incorrect filing, a missed information return, or a payroll-deposit problem.

Why did my business get a CP215?

Common reasons include filing a return like Form 941 or 940 late, not depositing payroll taxes on time, failing to file information returns such as W-2s or 1099s, or filing them late or with errors. The notice lists the specific Internal Revenue Code section and the period that triggered the penalty.

Can a CP215 penalty be removed?

Often, yes. If your business has a clean compliance history, first-time penalty abatement may remove it entirely. If the penalty was caused by circumstances beyond your control — illness, disaster, reliance on bad advice — reasonable-cause relief may apply. You can also dispute the penalty if the IRS's facts are wrong.

What happens if I ignore a CP215?

The penalty doesn't go away. Interest keeps building, and the balance moves into the IRS business collection sequence — reminder notices, then a Notice of Intent to Levy, then liens and levies against business assets or accounts. Acting before the pay-by date keeps the most options open.

Is a CP215 the same as the Trust Fund Recovery Penalty?

No. A CP215 is a civil penalty assessed against the business entity. The Trust Fund Recovery Penalty is assessed personally against owners or responsible people for unpaid payroll trust-fund taxes, and it arrives through a different process starting with Letter 1153. If you owe payroll taxes, both can be in play.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.