Local Tax Relief

Tax Relief in Fresno: Your Guide to IRS and California FTB Help (2026)

The short answer: tax relief in Fresno means resolving back taxes owed to both the IRS and the State of California through legitimate programs — payment plans, hardship status, penalty relief, or a settlement when you truly qualify. Because California's Franchise Tax Board collects aggressively, most Fresno residents need a plan that covers both agencies at once.

Owe the IRS or California and not sure where to start?

Tell us what letters you're holding. An experienced tax professional will map out both your federal and California options — free, confidential, and with zero pressure. We help Fresno and Central Valley residents every week.

⏱ Why timing matters: the IRS final levy notice gives you 30 days to act before wages or bank accounts can be taken. California moves on its own clock and can issue an Order to Withhold against your bank or an Earnings Withholding Order against your paycheck — often faster than the IRS. The sooner you respond, the more options you keep.

What tax relief actually means for Fresno residents

If you live in Fresno and owe back taxes, you're not alone, and you're not stuck. From the farming and ag-processing economy of the Central Valley to small businesses along the Tower District and self-employed workers across Clovis and the wider county, plenty of hard-working people fall behind — a bad year, a 1099 with no withholding, a return that never got filed.

Tax relief is not a magic eraser. It's the set of real, government-run programs that let you deal with a tax debt on terms you can actually live with: a monthly payment plan, a pause on collection when money is genuinely tight, removal of certain penalties, or — in the right cases — a settlement for less than the full balance. The goal is simple: stop the escalation, protect your paycheck and bank account, and get back to normal life.

The twist for Fresno is that "the tax man" is really two of them. You have the federal IRS, and you have the State of California — and California is one of the toughest tax collectors in the country.

The Fresno and California tax landscape

Here's the local picture, agency by agency.

The IRS (federal). Fresno is served by a local IRS Taxpayer Assistance Center that handles in-person help by appointment only. Don't just drive over — confirm the current address, hours, and appointment line through the official IRS local office locator. Honestly, most tax debt work — payment plans, transcripts, hardship requests — gets handled faster by phone, online, or through a representative than at a counter.

The California Franchise Tax Board (FTB). This is the state's income-tax collector, and it's the one that catches Fresno residents off guard. California has a high state income tax, and the FTB is unusually aggressive about collecting it. The FTB can:

- Issue an Order to Withhold — a bank levy that freezes and pulls money straight from your account;

- Issue an Earnings Withholding Order — a wage garnishment that takes a chunk of every paycheck;

- Push to suspend professional and occupational licenses and place holds on driver's license renewals for large balances;

- Pursue you for a 20-year collection statute — double the IRS's 10-year window.

You can look up exactly what an FTB letter means in our FTB notice decoder, and see the official rules straight from the source at the California Franchise Tax Board website.

CDTFA and EDD. If you run a business in Fresno, two more state agencies can come into play. The California Department of Tax and Fee Administration (CDTFA) handles sales and use tax — a real risk for restaurants, shops, and dealerships that collected sales tax but fell behind on remitting it. The Employment Development Department (EDD) handles state payroll tax, which becomes serious fast when employee withholding is involved. Both can levy and lien much like the FTB.

IRS vs. California: which to handle first

When you owe both the IRS and California, the order you tackle them in matters — and it's not always obvious.

The instinct is to chase the bigger number first, and the IRS balance is usually larger. But the right question isn't "who do I owe more?" — it's "who is about to take my money?" Because the FTB often moves faster and has a longer 20-year reach, a California garnishment or bank levy can hit your Fresno paycheck before the IRS finishes its notice sequence. If the state is already sending levy warnings, that fire usually gets put out first.

The two systems also interact. The IRS and FTB share data, so an issue with one frequently surfaces with the other. A federal installment agreement doesn't automatically cover your state balance, and vice versa — you generally need a separate arrangement with each. And California bases your state tax on your federal return, so fixing unfiled or amended federal returns can change what you owe the state.

To see how much of your paycheck is actually at risk, read how much the FTB can garnish, and for a deeper walk-through of sequencing both agencies, see our guide on FTB vs. IRS: which to handle first. The full state overview lives in our California tax debt relief guide.

A note for married Fresno couples: community property

California is a community-property state. In plain terms, income earned and debts taken on during a marriage are usually treated as shared — which means one spouse's tax debt can reach into the other spouse's wages and accounts, even on a balance only one of you created.

Two different protections exist, and people mix them up constantly:

- Innocent-spouse relief can remove your responsibility for tax that came from your spouse's errors or unreported income — when you didn't know and had no reason to know. See the IRS rules on innocent spouse relief.

- Injured-spouse relief protects your share of a joint refund when it's grabbed to pay your spouse's separate debt — like back taxes from before the marriage.

Which one fits depends entirely on your facts. If you're being pursued for a balance you feel isn't yours, this is worth a careful review before you pay a dime.

Common Fresno situations we help with

Most local cases fall into a handful of patterns. If you recognize yours, there's a known path forward:

- Self-employed and 1099 workers who didn't set aside enough for taxes and now owe both the IRS and FTB. An IRS payment plan plus a matching state arrangement usually stops the bleeding.

- Unfiled returns stacking up over several years. We get the returns filed first — often lowering the balance the agencies estimated for you — through our unfiled returns help.

- FTB or IRS garnishment hitting a paycheck. When money is genuinely too tight to pay, Currently Not Collectible status can pause IRS collection, with a parallel hardship request to the state.

- Real settlement candidates. If your income and assets truly can't cover the debt, an Offer in Compromise may let you resolve it for less. The IRS sizes the offer using your Reasonable Collection Potential — basically what it could collect from your assets and future income. Want a ballpark before committing? You can estimate your own offer with our Offer in Compromise Calculator, which estimates the lowest amount the IRS may accept. California runs its own separate offer program.

Be wary of anyone promising to settle your debt for pennies on the dollar before they've even looked at your finances — that's a sales pitch, not a strategy. Browse our full tax relief services to see how each program works.

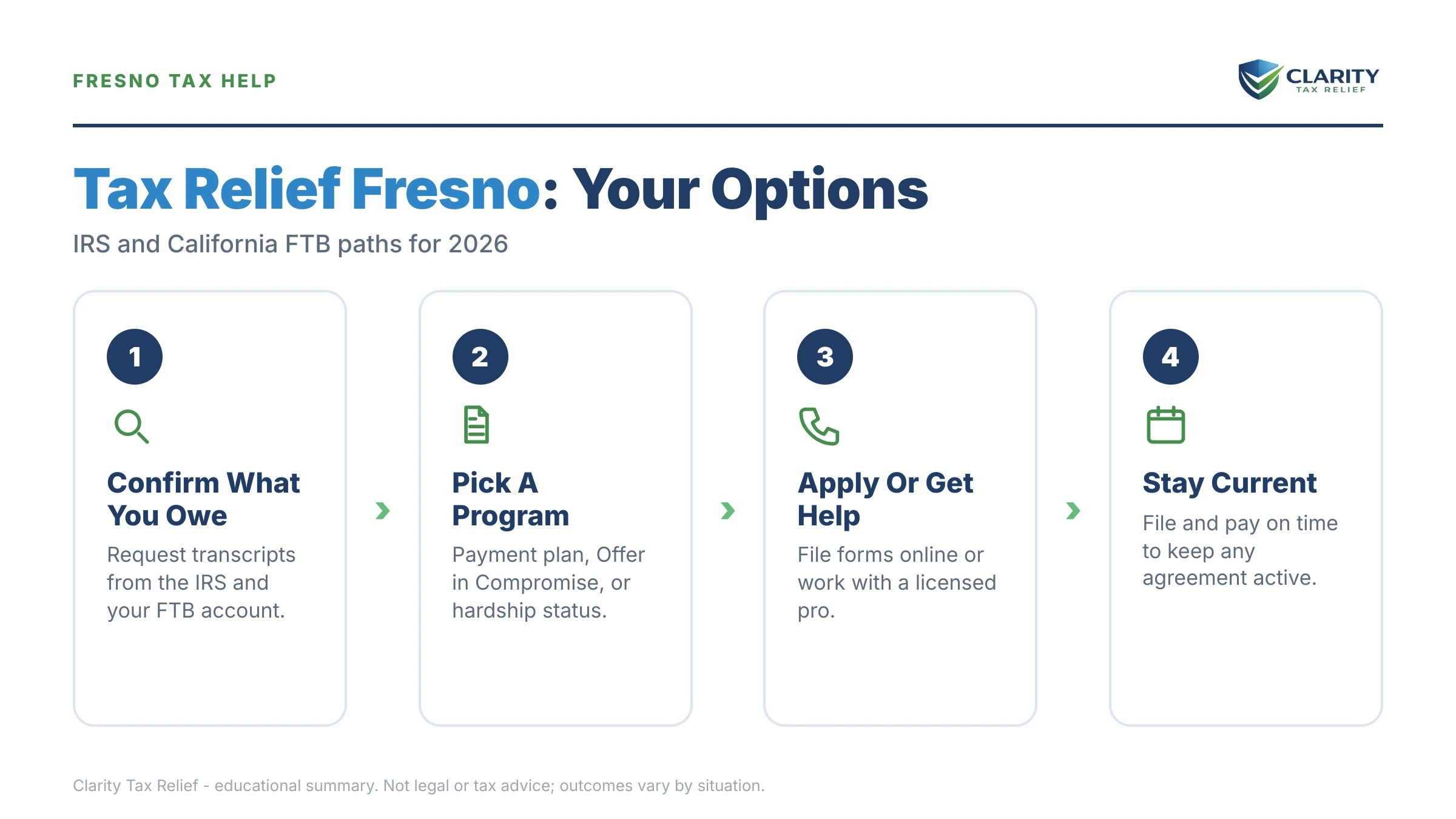

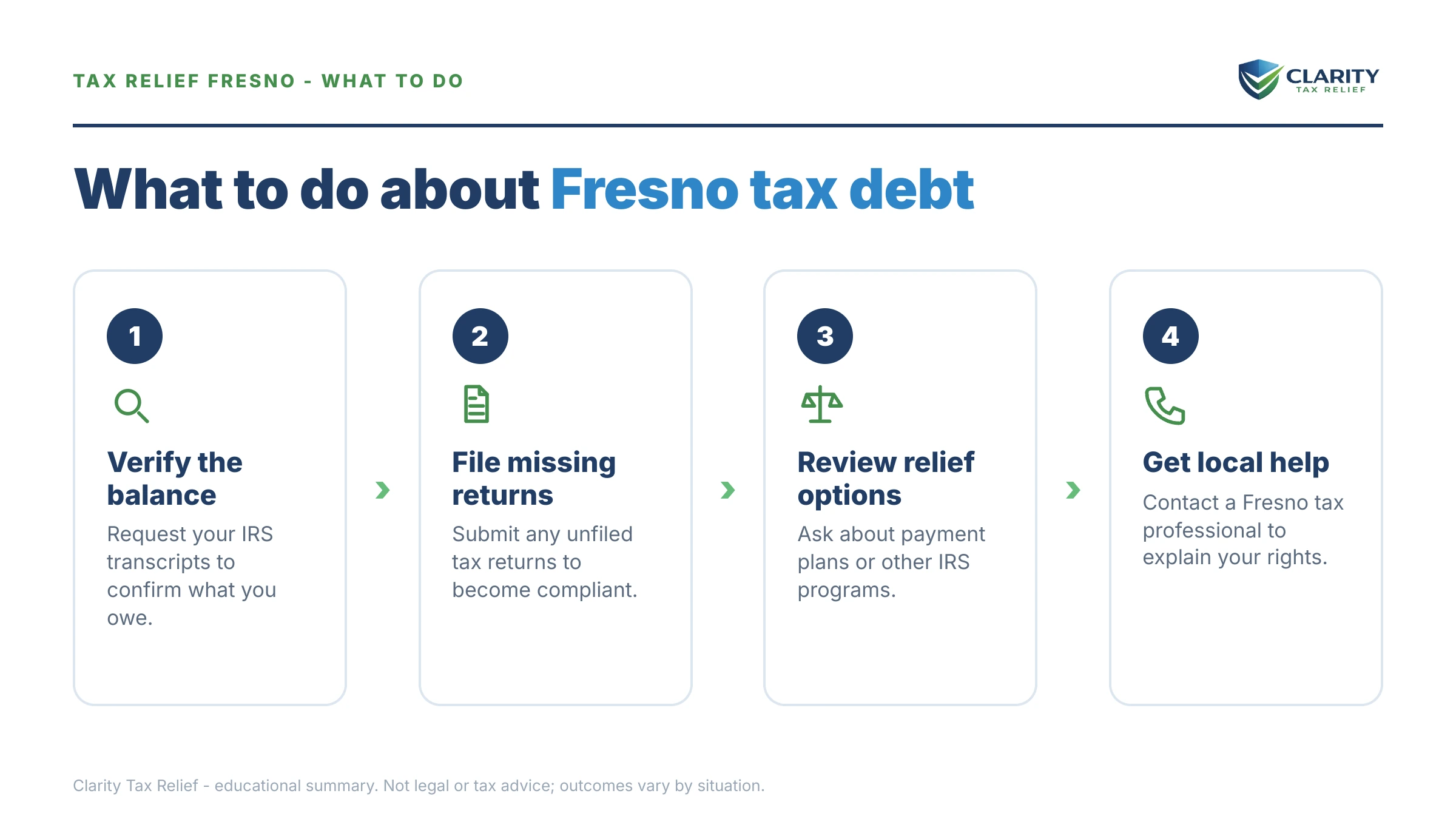

How to respond, step by step

- Open every letter and sort by agency. Separate IRS notices from FTB, CDTFA, and EDD letters. The deadlines are different for each.

- Find the most urgent deadline. A "final notice of intent to levy" or any garnishment warning — federal or state — goes to the top of the pile.

- Verify the balances. Check your IRS online account and your FTB account so you're working from real numbers, not just the letter.

- File any missing returns first. You generally can't set up a plan or settlement until all required returns are filed.

- Choose a resolution for each agency. Payment plan, hardship status, penalty relief, or settlement — usually one with the IRS and a separate one with California.

- Get a professional review if you owe more than $10,000 or owe both agencies. The order you fix things in changes what you ultimately pay.

Fresno tax relief questions, answered

Is there a local IRS office in Fresno?

Yes. Fresno is served by an IRS Taxpayer Assistance Center, which handles in-person help by appointment only. Don't just show up — find the current location, hours, and the appointment line through the official IRS office locator at irs.gov/help/contact-your-local-irs-office. Many tax debt issues can be handled by phone or online without visiting at all.

Should I pay the IRS or the California FTB first if I owe both?

It depends on who is moving against you fastest. The California Franchise Tax Board often collects more aggressively than the IRS, with bank levies and wage garnishments that hit quickly, plus a 20-year collection window versus the IRS's 10 years. But the IRS balance is usually larger. An experienced tax professional can review both and build a strategy that protects your paycheck and bank account first.

Can the California FTB really suspend my driver's license over taxes?

Yes. California is unusually aggressive. The FTB can have professional licenses suspended and can place a hold on driver's license renewals for large unpaid balances, on top of bank levies through Orders to Withhold and paycheck garnishments through Earnings Withholding Orders. Acting before these tools are used gives you far more options than waiting.

My spouse owes back taxes — am I responsible in California?

California is a community-property state, so income and debts during the marriage are often shared, which can expose a spouse to the other's tax debt. Innocent-spouse relief may remove your responsibility for tax your spouse caused, while injured-spouse relief protects your share of a refund taken for your spouse's separate debt. Which applies depends on your facts.

Can I really settle my Fresno tax debt for less than I owe?

Sometimes — through an IRS Offer in Compromise or an FTB offer in compromise — but only when your income and assets genuinely can't cover the debt. Anyone promising to settle for pennies on the dollar before reviewing your finances is selling you something. The agencies run the math, and a professional can tell you whether you actually qualify.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.