Local Tax Relief

Tax Relief in Oakland: IRS and California FTB Help (2026)

The short answer: tax relief in Oakland means getting your IRS and California Franchise Tax Board (FTB) debt under control — through payment plans, hardship status, penalty relief, or a settlement offer. Because California collects more aggressively than the IRS and for twice as long, Oakland residents usually need a plan that handles both at once.

Owe the IRS, the FTB, or both?

Tell us what notices you're holding. An experienced tax professional will map out where you stand with each agency and what options may fit your situation — free, confidential, and no pressure.

Why Oakland residents face a double tax problem

Oakland sits in one of the most expensive corners of the country. Between Bay Area rents, a high cost of living, and gig and contract work that doesn't withhold taxes, it's easy for a tax bill to grow faster than a paycheck. When that happens here, you're not dealing with one tax agency — you're dealing with two.

That's the part most online guides skip. If you owe the IRS, you very likely owe California too, because the state taxes the same income at some of the highest rates in the nation. Real tax relief in Oakland has to account for both the federal bill and the state one, because the rules they each follow are very different.

What tax relief actually means for people who live here

"Tax relief" is not a magic eraser. It's a set of legal programs that change how you pay what you owe — or, in some cases, how much. For an Oakland household, that usually looks like one of these:

- A monthly payment plan with the IRS, the FTB, or both, so collection stops while you pay over time.

- Currently Not Collectible status with the IRS — a pause on collection when paying anything would leave you unable to cover rent and basics. The FTB has a similar hardship status.

- Penalty relief, such as first-time abatement, that removes failure-to-pay penalties when you have a clean prior record.

- An offer to settle for less than the full balance — available, but only when your finances genuinely support it.

Anyone promising to settle your debt for "pennies on the dollar" before they've reviewed your income, assets, and both tax balances is selling you something. The honest version of this work starts with your numbers, not a headline.

The local and state tax landscape: IRS, FTB, CDTFA, and EDD

The IRS handles your federal income tax. Oakland is served by a local IRS Taxpayer Assistance Center, and most visits require an appointment. Don't trust an address or phone number from a letter, email, or text — confirm the current details using the official IRS local office locator.

California has three separate tax agencies, and which one you're dealing with depends on the type of tax:

- The California Franchise Tax Board (FTB) collects state personal income tax. For most Oakland residents, this is the state agency you'll hear from. Start with the official California Franchise Tax Board website.

- The California Department of Tax and Fee Administration (CDTFA) collects sales and use tax — important if you run a shop, restaurant, or online business.

- The Employment Development Department (EDD) collects state payroll taxes from employers.

Here's what makes California different — and why this isn't a generic problem. The FTB collects far more aggressively than the IRS. It can issue an Order to Withhold, which freezes and sweeps your bank account, and an Earnings Withholding Order to garnish your wages. For larger debts, California can move to suspend professional licenses and even driver's licenses. And the FTB has a 20-year collection statute — double the IRS's 10-year window. A federal debt may eventually expire; the state version can follow you for two decades.

⏱ Don't sit on a state notice: the IRS generally sends several reminder notices before it levies. The FTB can move faster. If you've received an FTB Final Notice Before Levy, an Order to Withhold can hit your bank account in a matter of weeks. Acting early is the difference between a plan you choose and a levy you don't.

IRS vs. FTB: which do you handle first?

When you owe both, the order matters. There's no single right answer, but these principles guide the strategy for most Oakland clients:

- Whoever is levying comes first. If the FTB has frozen your bank account or the IRS has sent a final notice of intent to levy, that agency is the immediate fire to put out.

- Don't let the state slide just because it feels smaller. The 20-year California collection window means a state balance you ignore now can resurface for decades. The IRS clock runs only 10 years.

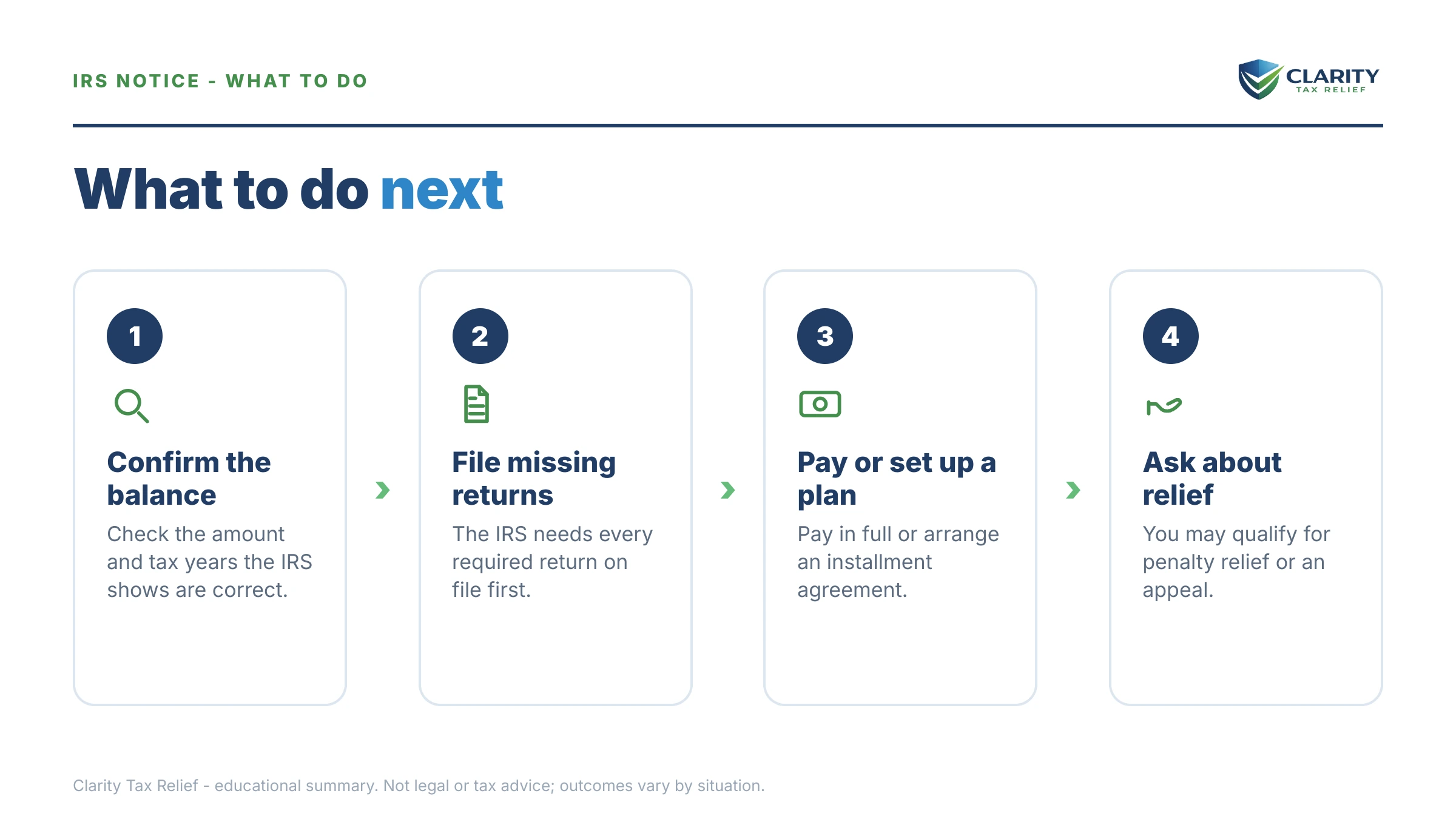

- File everything first. Neither agency will approve a payment plan or settlement while returns are missing. If you have unfiled years, that's step one for both.

- Coordinate the two plans. The IRS and FTB don't talk to each other about your budget. A plan that satisfies one can leave you unable to pay the other. The numbers have to work together.

We walk through this in more detail in our guide on FTB vs. IRS — which to handle first, and you can learn how state garnishment works in how much the FTB can garnish. If a California notice has you confused, the FTB notice decoder explains what each one means.

Married and owe? California's community-property rule

California is a community-property state. That means income earned and many debts taken on during a marriage are generally treated as shared — even if only one spouse's name is on the tax return or the income. For Oakland couples, this raises a real question when one spouse owes back taxes.

Two different forms of relief can apply, and people mix them up constantly:

- Innocent-spouse relief may remove your responsibility for tax your spouse (or former spouse) underreported, when you didn't know and had no reason to know about it. The IRS explains the rules on its innocent spouse relief page.

- Injured-spouse relief is different — it's for when your joint refund gets taken to pay a debt that belongs only to your spouse, like their separate back taxes or child support. It can help you recover your share of that refund.

In a community-property state, these claims get more complicated, not less. If your tax problem traces back to a spouse, get it reviewed before you assume you're stuck with the bill.

Situations we help Oakland residents with

- An FTB bank levy (Order to Withhold) that froze an account with rent money in it.

- Wage garnishment from an FTB Earnings Withholding Order or an IRS levy on a Bay Area paycheck.

- Self-employed and gig workers — rideshare drivers, contractors, freelancers — who fell behind because no one withheld taxes for them.

- Small business owners facing CDTFA sales-tax bills or EDD payroll-tax problems on top of income tax.

- Years of unfiled returns with both the IRS and the state, which must be filed before any relief begins. Our guide to California tax debt relief covers this in depth.

- Hardship cases where high Oakland living costs leave nothing left to pay either agency — a possible fit for Currently Not Collectible status.

Depending on your numbers, the right path might be an IRS payment plan, penalty relief, or an Offer in Compromise. You can also browse all of our tax relief services to see how the process works from start to finish.

How to take the first step

- Gather your notices. Put every IRS and FTB letter in one place and note the dates.

- Check your accounts online. Confirm your real federal balance through your IRS online account and your state balance on the FTB site.

- Find any unfiled years. You can't get relief from either agency until your returns are filed.

- Stop the most urgent threat first — usually whichever agency is closest to a levy or garnishment.

- Get a professional review before you commit to any single agency's plan, so the two solutions fit together.

Oakland tax relief questions, answered

Should I deal with the IRS or the California FTB first if I owe both?

It depends on who is moving against you. The agency that has issued a levy, garnishment, or final notice usually comes first because it can take your money soonest. But remember the California Franchise Tax Board has a 20-year collection window versus the IRS's 10 years, so the state problem rarely just goes away. An experienced tax professional can look at both balances and build one plan that covers them together.

Can the California FTB really suspend my driver's license over taxes?

Yes. California is unusually aggressive. The FTB can issue Orders to Withhold to freeze your bank account, send Earnings Withholding Orders to garnish your wages, and refer certain large tax debts for suspension of professional and driver's licenses. This is one reason Oakland residents should not ignore state notices, even when the IRS feels like the bigger threat.

I live in Oakland and my spouse owes back taxes — am I on the hook?

Maybe. California is a community-property state, so income and many debts during marriage can be treated as shared. If the debt came from your spouse's actions and you did not know about it, you may qualify for innocent-spouse relief, which can remove your responsibility. If a joint refund was taken to pay your spouse's separate debt, injured-spouse relief may get your share back. The two are different, and which one fits depends on the facts.

Is there an IRS office in Oakland I can visit?

Oakland is served by a local IRS Taxpayer Assistance Center, and most in-person help requires an appointment. Use the official IRS office locator at irs.gov/help/contact-your-local-irs-office to confirm the current address, hours, and phone number before you go. Always verify these details on IRS.gov rather than trusting a number from a letter, email, or text.

Can I settle my tax debt for less than I owe in California?

Sometimes. Both the IRS and the California FTB have offer programs that may let you pay less than the full balance when your income and assets genuinely cannot cover the debt. Approval is based on a detailed look at your finances — no one can promise a result before reviewing them. Anyone guaranteeing to settle for pennies on the dollar before seeing your numbers is selling you something.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.