State Back Taxes

Maryland Comptroller Back Taxes: What They Are and How to Resolve Them (2026)

The short answer: Maryland Comptroller back taxes are unpaid state (and county) income, sales, or withholding taxes collected by the Comptroller of Maryland. Resolve them by paying in full, a payment agreement, Maryland's Offer in Compromise, or hardship deferral — acting before your notice's response date prevents wage liens and license renewal holds.

The return address says Comptroller of Maryland, Compliance Division — and the balance inside landed in the middle of a year when you're already rebuilding everything else. Here's what matters: Maryland's collection system is smaller than the IRS's but moves faster in the ways that hurt, and every one of its enforcement tools has a release path if you act before the response date on your notice.

This guide covers why the Comptroller assessed you, what happens at each stage if you do nothing, and every resolution option Maryland actually offers — with the eligibility rules and costs the notice itself never explains. The image below shows what a Maryland Comptroller collection notice looks like and where to find the notice number, tax year, balance, and response date that control everything that follows.

⏱ Your deadline: the response date printed on your Maryland notice controls your options. There is no grace period after it — interest and penalties keep accruing monthly, and each enforcement stage that follows (refund intercept, recorded lien, wage lien, license renewal hold) is harder to unwind than the one before it.

Why the Comptroller of Maryland is contacting you

The Comptroller of Maryland is the state's tax collector, and it pursues back taxes for one of four core reasons: a filed return with an unpaid balance, a mismatch between your federal and Maryland returns, an unfiled Maryland return, or unpaid business trust taxes.

You filed but didn't pay in full. This is the most common trigger. You filed your Form 502, the payment didn't cover the balance, and the Comptroller's billing cycle started. Penalties and interest have been stacking on top since the original due date — which is why the number on the notice is bigger than the number on your return.

Your federal and Maryland numbers don't match. Maryland receives federal return data from the IRS. If the IRS adjusted your federal return — a CP2000 underreporter change, an audit, an amended return — the Comptroller typically follows with its own assessment for the Maryland tax on that same income. Many Marylanders resolve the IRS side and are blindsided months later when the state's bill for the identical issue arrives.

You didn't file a Maryland return at all. If W-2s or 1099s show Maryland income and no return was filed, the Comptroller can estimate an assessment for you. Estimated assessments ignore your deductions, exemptions, and correct filing status, so they usually overstate what you'd owe on a real return. Filing the actual return is often the single biggest reduction available.

Your business owes trust taxes. The Comptroller also collects sales and use tax and employer withholding — money collected from customers or employees and held in trust for the state. These debts carry personal exposure for the people responsible, and the state treats them as its most urgent collection priority.

One Maryland-specific wrinkle worth knowing: your Maryland bill includes the county (or Baltimore City) local income tax, collected on the same return. That piggyback local tax is why Maryland balances often feel larger, relative to income, than people expect — and why a filing-status change after a divorce can produce a surprisingly big swing.

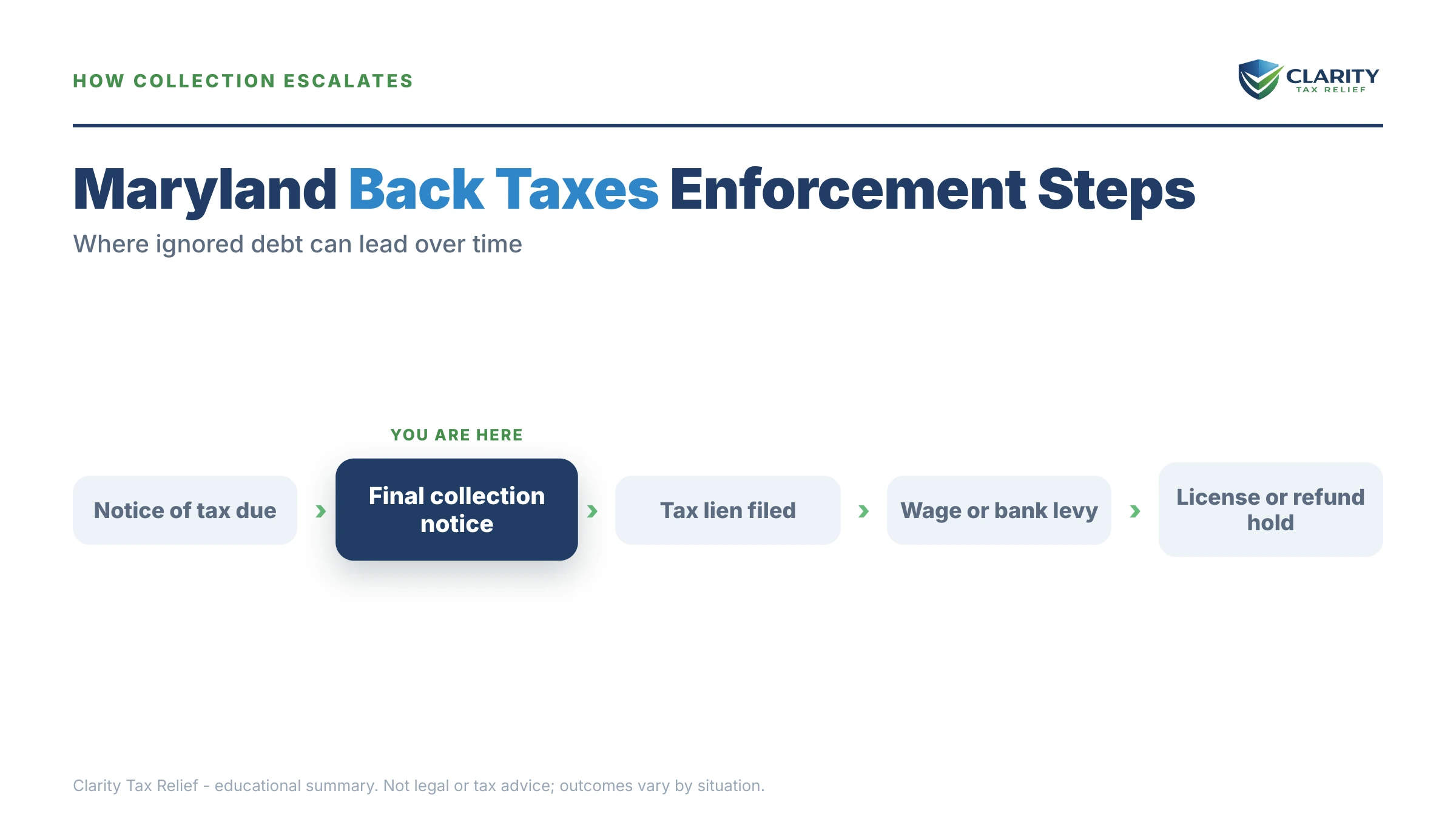

What happens if you ignore Maryland back taxes

Ignoring Comptroller of Maryland notices leads to refund intercepts, a court-recorded tax lien, wage liens, bank attachments, and renewal holds on your driver's license and vehicle registration — in roughly that order. The sequence is largely automated; it does not require a human to decide your file is worth pursuing.

- Assessment and billing. The first notice states the tax year, balance, and response date. Penalties and interest are already accruing.

- Follow-up demands. Continued non-response brings escalating demand notices while the balance grows every month.

- Refund intercepts. Your Maryland refund is applied to the debt automatically, and the state can certify the debt to the federal Treasury Offset Program to take your federal refund too.

- Tax lien recorded in circuit court. A Maryland tax lien functions like a court judgment: it's public record, attaches to your property, and complicates selling or financing a home.

- Wage lien or bank attachment. The Comptroller can send a wage lien directly to your employer — no lawsuit required — taking a slice of every paycheck. It can also attach funds in your bank account.

- License and registration holds. The state can flag your account with the Maryland Motor Vehicle Administration, blocking renewal of your driver's license and vehicle registration, and can hold professional license renewals as well.

- Outside collection referral. In some cases the Comptroller refers stale accounts to an outside collection agency, which can add collection costs on top of everything else.

Unlike the IRS, Maryland's clock offers little rescue. The IRS's collection statute generally expires 10 years after assessment; Maryland's collection window runs far longer, and a recorded lien behaves like a judgment. Waiting out the Comptroller is not a plan — confirm your account's specific dates with the Comptroller's office rather than assuming any expiration.

| Enforcement tool | What it does | How to stop or release it |

|---|---|---|

| State refund intercept | Your Maryland refund is applied to the debt automatically | Resolve the balance; refunds typically keep offsetting until it's paid |

| Federal refund offset (Treasury Offset Program) | Your federal refund is taken and sent to Maryland | A pre-offset notice comes first — pay, arrange, or file a spousal claim for a non-liable spouse's share |

| Tax lien recorded in circuit court | Public judgment that attaches to property and blocks clean financing | Pay or settle the debt, then confirm the release is recorded |

| Wage (salary) lien | Your employer must send part of each paycheck to the state | A payment agreement or documented hardship is the usual release path |

| Bank account attachment | Funds in the account are frozen and taken | Act before it lands — releases after attachment are difficult |

| License & registration renewal holds | Driver's license, vehicle registration, and professional license renewals blocked | Enter an approved arrangement; the flag lifts once you're compliant |

Holding a Comptroller of Maryland notice right now?

The stage after billing is enforcement — refund intercepts, a recorded lien, a wage lien to your employer. Get your Maryland notice reviewed free before the response date printed on it passes. An experienced tax professional will decode exactly where your account stands and which option fits your finances.

How to resolve Maryland Comptroller back taxes: your options

Maryland offers five real resolution paths — full payment, a payment agreement, an Offer in Compromise, hardship deferral, and penalty relief — plus appeal rights if you dispute the assessment itself. Which one fits depends on your finances, not your preference.

| Option | Best for | Key eligibility / what to know |

|---|---|---|

| Pay in full | You can raise the money without hardship | Fastest, cheapest end to the case; stops all accrual and enforcement |

| Payment agreement | Steady income and a balance you can retire over time | All required returns must be filed; missed payments can void the agreement |

| Offer in Compromise | Income and assets genuinely can't cover the debt | Means-tested; full financial disclosure required; declined if a plan could pay it |

| Hardship deferral | Paying anything would prevent basic living expenses | Temporary; the balance keeps growing and the state revisits your finances |

| Penalty waiver | A cause beyond your control led to the late filing or payment | Removes penalties only, not tax; document the cause in writing |

| Appeal / hearing | You dispute that you owe the assessed amount at all | Strict appeal window that starts on the notice date — check your notice |

Maryland payment agreement

A payment agreement is the workhorse resolution for Maryland individual income tax debt. Smaller balances can often be set up online or by phone with minimal paperwork; larger balances and business trust taxes usually require talking to the Compliance Division, and the state may ask for financial disclosure before approving terms. Interest continues to accrue during the plan, so a shorter term always costs less in total — and staying current on every future Maryland filing is a condition of keeping the agreement alive.

Maryland Offer in Compromise

Maryland runs its own Offer in Compromise program, separate from the IRS's. It can settle a state tax debt for less than the full balance on two grounds: your documented finances show the state could never collect it in full, or there's genuine doubt you owe it. Expect full disclosure of income, expenses, and assets, and expect a decline if the numbers show a payment plan could retire the debt. It's a real program, but a means-tested one — not a discount anyone can request.

Hardship deferral

If paying anything would leave you unable to cover rent, food, or medical care, the Comptroller can temporarily suspend active collection while your situation improves. Two honest caveats: the debt remains and keeps growing with interest, and refund intercepts typically continue even while collection activity is paused. Hardship status buys breathing room; it doesn't resolve anything by itself.

Penalty waiver

Maryland can waive penalties when a circumstance beyond your control caused the late filing or payment — serious illness, a disaster, records tied up in litigation, or a life event like a divorce that genuinely disrupted your finances. Put the request in writing, attach documentation, and be specific about dates. Interest is rarely waived, so treat penalty relief as a meaningful reduction, not a reset. (Note that Maryland's rules are its own — federal programs like first-time abatement don't apply to a state balance.)

Disputing the assessment

If the assessment itself is wrong — the income isn't yours, the estimated assessment ignores your real return, or the federal adjustment it's based on was reversed — you can request an informal hearing with the Comptroller's hearings and appeals staff, and appeal further to the Maryland Tax Court if needed. The appeal window is short and starts on the notice date, so check your specific notice and don't let the deadline pass while you gather documents.

| Option | What it costs you | Typical timeline |

|---|---|---|

| Pay in full | The balance shown plus interest accrued through payoff | Immediate; ends penalties, interest, and enforcement |

| Payment agreement | Full balance over time; interest keeps accruing during the plan | Setup often within days; payoff runs the length of the plan |

| Offer in Compromise | The offered amount if accepted, plus time and documentation to prepare | Months for review; interest accrues while it's pending |

| Hardship deferral | Nothing now, but the balance keeps growing and refunds are still intercepted | Relief while approved; the state periodically re-reviews your finances |

| Penalty waiver | Free to request; removes penalties, not tax or (usually) interest | Weeks to months for a written decision |

| Appeal / hearing | Free to request; professional representation optional | Short window from the notice date; hearing first, Maryland Tax Court after |

A worked example: say you owe Maryland $19,700 after a divorce

Say your divorce was final in March, your withholding was still set for married-filing-jointly all year, and your first single-filed Maryland return — state plus county local tax — lands with a $19,700 balance you don't have. This is hypothetical, but the math is real:

- Do nothing: penalties and interest compound monthly, this year's state and federal refunds get intercepted, and the eventual wage lien takes the decision out of your hands at a percentage you don't choose.

- 24-month payment agreement: $19,700 ÷ 24 ≈ $821/month before interest — heavy on one income, but it ends the case in two years with the least total interest.

- 48-month payment agreement: $19,700 ÷ 48 ≈ $410/month before interest — livable on a post-divorce budget, at the cost of more total interest over the longer term.

- Offer in Compromise: only if the disclosure math supports it. If your take-home is $4,000/month and allowable expenses leave roughly $600/month free, the state sees a taxpayer who can pay through a plan — and will say so. An offer fits when income and assets genuinely can't reach $19,700, not when a plan merely feels painful.

Then fix the leak: update your Maryland withholding for single status so next April doesn't create a second balance behind this one.

Divorced and holding a joint Maryland tax bill

On a joint Maryland return, both spouses are liable for the entire balance — and your divorce decree does not change that. A decree assigning the tax debt to your ex is enforceable between the two of you in family court, but the Comptroller isn't a party to it and can collect 100% from whichever spouse is easier to reach. The same principle applies federally; see why a divorce decree doesn't bind tax collectors and divorce and IRS debt: who pays.

What you can do on the Maryland side:

- Protect your own refunds. If you've remarried, a claim for the non-liable spouse's share can protect part of a joint refund from being swallowed by your old debt — but it must be filed; nothing happens automatically.

- Raise the underreporting issue. If your ex hid income or overstated deductions without your knowledge on a joint return, relief from the resulting liability may be available. Document what you knew and when.

- Get your own agreement. If your ex won't cooperate, don't wait — the state won't split enforcement fairly between you. An agreement in your name protects your paycheck and your license renewal regardless of what your ex does.

If you owe Maryland and the IRS both

Owing both agencies is common — the same underreported income or unpaid balance usually creates two bills. The general framework for sequencing them lives in our guide to state tax debt vs. IRS: which to resolve first. The Maryland-specific reality: the Comptroller often reaches enforcement faster than the IRS's long notice sequence, and the two agencies raid each other's refunds — Maryland certifies debts to take your federal refund, and the IRS can grab your state refund through its own levy program. If a refund already vanished and you're not sure who took it, start with state refund taken for tax debt. The workable answer is almost always two affordable arrangements, prioritizing whichever agency has already threatened or begun enforcement.

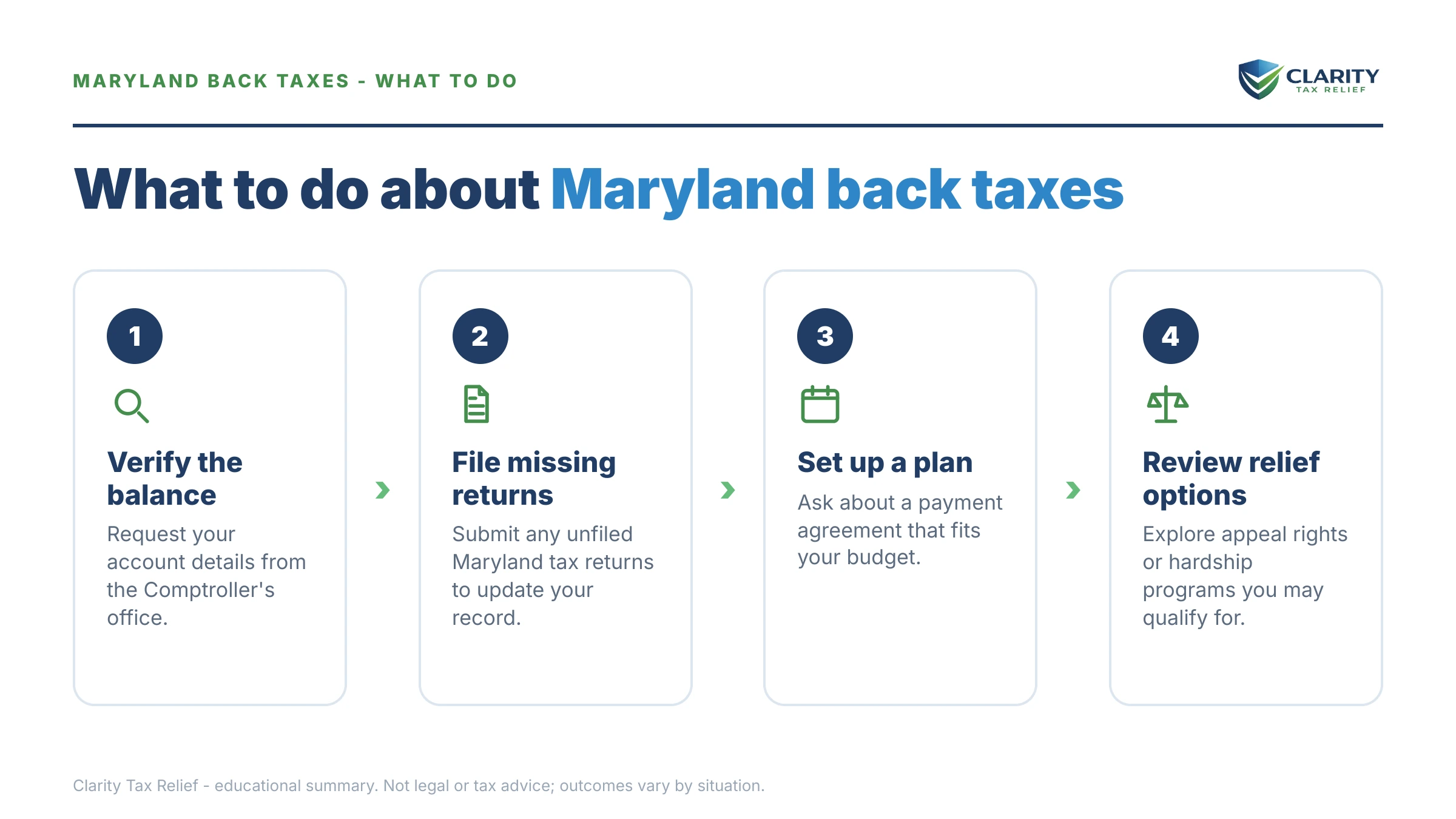

How to respond to a Maryland Comptroller collection notice, step by step

- Verify the balance. Contact the Comptroller's Compliance Division or check your account through the state's online services to confirm the tax years, the amounts, and how much of the balance is penalty and interest versus tax.

- File any missing Maryland returns. The Comptroller generally won't approve a payment agreement or an offer while required returns are unfiled — and filing can replace an estimated assessment with your real, often lower, number.

- Choose your resolution path. Pay in full if you can, request a payment agreement if you need time, or pursue an Offer in Compromise or hardship deferral if your documented finances support it.

- Set it up before your response date. An approved arrangement stops the escalation to liens, wage liens, and license holds; a missed deadline restarts it.

- Request penalty relief in writing. If illness, the divorce itself, or another circumstance beyond your control caused the late filing or payment, ask for a penalty waiver and attach documentation.

- Get a professional review if enforcement has started. Once a lien is recorded or a wage lien is issued, the order you fix things in — returns, penalties, then the balance — changes what you end up paying.

When you can handle Maryland back taxes yourself

You likely don't need professional help if the balance is one you can pay within a few months, it covers a single tax year, you agree with the number, and no enforcement has started. Verify the balance, set up the payment agreement, keep every confirmation, and stay current going forward — that's the whole job, and paying someone to do it adds cost without changing the outcome.

Experienced help changes outcomes in specific situations: a wage lien already at your employer or a lien already recorded in circuit court; multiple unfiled Maryland years sitting under estimated assessments; business trust-tax exposure like sales tax debt or withholding, where personal liability is on the table; a joint-liability fight after divorce; or an Offer in Compromise, where the disclosure package is won or lost on how the financial math is presented. In those cases the sequencing — which returns to file first, which relief to request before which agreement — routinely changes the final number.

If your Maryland case involves a recorded lien, a wage lien, or years of unfiled returns, get a free case review before the next notice lands — or call (888) 825-7779.

Terms on your Maryland notice, decoded

- Assessment — the formal act of putting a tax debt on the books; the notice date and assessed amount flow from it.

- Salary (wage) lien — Maryland's administrative wage garnishment: an order sent straight to your employer, no lawsuit required.

- Judgment lien — a Maryland tax lien recorded in circuit court, giving the state the powers of a judgment creditor against your property.

- Refund intercept / offset — your state or federal refund applied to the debt before you ever see it.

- License hold — a flag with the MVA or a licensing board that blocks renewal of your driver's license, registration, or professional license until you're compliant.

- Maryland Tax Court — the independent body that hears appeals when you and the Comptroller disagree after an informal hearing.

Maryland Comptroller back taxes: FAQs

Can the Comptroller of Maryland stop me from renewing my driver's license?

Yes. The Comptroller can flag unpaid tax accounts with the Maryland Motor Vehicle Administration, which blocks renewal of your driver's license and vehicle registration until the debt is resolved or you enter an approved payment arrangement. It's a renewal hold, not an immediate suspension — but it surfaces at the worst moment, when your renewal is due. Entering a payment agreement is usually the fastest way to get the flag lifted.

Does Maryland tax debt expire like IRS debt does?

Not on the same schedule. The IRS generally has 10 years from assessment to collect, but Maryland's collection window runs far longer, and a recorded Maryland tax lien functions like a court judgment. Waiting out the Comptroller is not a realistic strategy for most people. Confirm the assessment dates on your specific account with the Comptroller's office or an experienced tax professional before making any decision based on timing.

Can Maryland garnish my wages without taking me to court?

Yes. The Comptroller can issue a wage lien directly to your employer through an administrative process — it does not need to sue you and win a judgment first, the way most private creditors do. Once your employer receives the lien, a portion of every paycheck goes to the state until the balance is paid or you negotiate a release, usually by entering a payment agreement.

Will Maryland take my federal tax refund for state back taxes?

It can. Maryland participates in the federal Treasury Offset Program, which lets the state intercept your federal income tax refund and apply it to certified state tax debt. The Comptroller also applies your Maryland state refund to the balance automatically. If part of the refund belongs to a new spouse who doesn't owe, an injured-spouse-type claim may protect their share — but you have to file it.

Does Maryland have an Offer in Compromise program?

Yes. The Comptroller's Offer in Compromise program can settle a Maryland tax debt for less than the full balance when your finances show you genuinely cannot pay it in full, or when there's real doubt you owe it. It is means-tested: you must document income, expenses, and assets, and offers from people who could pay through a payment plan are routinely declined. It's worth pursuing only when the financial math actually supports it.

My ex-spouse caused the debt — am I still liable on our joint Maryland return?

If you signed a joint Maryland return, you and your ex are each liable for the entire balance, and a divorce decree assigning the debt to one of you does not bind the Comptroller. The state can collect 100% from whichever spouse is easier to reach. Relief may be available if your ex understated income without your knowledge, and separate claims can protect your share of a refund — but you must request them; nothing happens automatically.

Should I pay Maryland or the IRS first if I owe both?

Usually you address whichever agency is closest to enforcement, and in many cases that's Maryland — the Comptroller can intercept refunds, issue wage liens, and hold license renewals with less lead time than the IRS's multi-notice sequence. That said, both balances accrue interest, so the practical answer is to get both into arrangements you can afford, prioritizing the one that has already threatened or started enforcement.

Can I set up a Maryland tax payment plan online?

In many cases, yes. The Comptroller offers online payment-agreement setup for individual income tax balances, and phone setup is available if your situation doesn't fit the online tool. Larger balances or business trust taxes like sales and withholding tax typically require speaking with the Compliance Division and may require financial disclosure before terms are approved. Missing a payment can void the agreement, so pick a number you can sustain.

What happens if I ignore Comptroller of Maryland collection notices?

The account escalates through a predictable sequence: continued billing with growing penalties and interest, interception of your state and federal refunds, a tax lien recorded in circuit court, then a wage lien or bank attachment, plus renewal holds on your driver's license, vehicle registration, and professional licenses. Each stage is harder to reverse than the one before it, which is why the cheapest moment to act is the notice you're holding now.

Your next 24 hours

- Find the controls on your notice: the notice number, tax year(s), total balance, and the response date. Those four items determine which options are still open.

- Gather your paperwork: the notice itself, your last two Maryland returns (the joint years and your first single-filed year), and your current income information — pay stubs or 1099s.

- Get a free case review before the response date on your notice passes: the 2-minute form or (888) 825-7779. An experienced tax professional will confirm what Maryland's records show and match your finances to the right resolution — payment agreement, offer, hardship, or appeal.

Primary sources: the Comptroller's official site at the Comptroller of Maryland handles payments, agreements, and account questions for state tax debt; if you also owe federally, the IRS's own options live at IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.