State Tax Debt

NJ Certificate of Debt: What It Means and How to Remove It (2026)

The short answer: a NJ certificate of debt is a judgment the New Jersey Division of Taxation dockets with the Superior Court — no lawsuit required. It creates a statewide lien, allows bank levies and wage executions, and stays enforceable for decades. You remove it by paying, negotiating, or contesting the assessment, then confirming a warrant of satisfaction is filed.

The Superior Court docket says the State of New Jersey holds a judgment against you — and you never set foot in a courtroom. Maybe you rent and assumed a "lien" couldn't touch someone without property; then a levy warning showed up anyway. Take a breath: a certificate of debt is a paperwork problem with a defined exit, and the order you act in matters more than the number.

Unlike an IRS notice, a certificate of debt has no response coupon and no "pay by" date. The visual guide below maps the deadlines and options, and points to the details — the docket number, tax periods, and judgment amount — that you'll need for every call you make about it.

⏱ The clock on a certificate of debt: there is no response window printed on it — the deadline that mattered was the 90-day window to protest the assessment behind it, and docketing usually means that window has closed. The clock running now is different: interest and collection fees accrue continuously, and enforcement can begin at any time.

Why New Jersey filed a certificate of debt against you

Under N.J.S.A. 54:49-12, the New Jersey Division of Taxation can convert an unpaid tax assessment into a court-docketed judgment without ever suing you. The Division simply files the certificate of debt (COD) with the Clerk of the Superior Court in Trenton, and from that moment it carries the same force and effect as a judgment a creditor won at trial.

The debt underneath the COD can be almost any New Jersey tax: gross income tax you filed but didn't pay, sales tax from a business, an estimated assessment the Division created for a year you never filed, or an adjustment after a federal change flowed through to your state return. If a year was estimated, the judgment amount may be far higher than what you actually owe — the Division assesses aggressively when it has to guess, and only a real return corrects the number. In some cases, amending a return to lower a tax debt is the fastest way to shrink the judgment itself.

Two facts surprise nearly everyone holding one. First, no court hearing happens before a COD is docketed — your appeal rights lived at the assessment stage, generally 90 days from the final assessment notice. Second, it reaches renters just as hard as homeowners: a judgment doesn't need real estate to attach to before the state pursues your paycheck and bank account.

What happens if you ignore a NJ certificate of debt

A docketed certificate of debt does not sit quietly — it is the launch point for every judgment-enforcement tool New Jersey has. The sequence runs like this:

- Final assessment. The Division bills you; the roughly 90-day protest window opens and closes. Most people who end up with a COD never responded at this stage.

- COD docketed with the Superior Court. The debt becomes a public-record judgment and a lien on any real or personal property you own in New Jersey. Title searches and lender background checks will find it.

- Referral to a contracted collection agency. New Jersey refers docketed debts to a private collector (Pioneer Credit Recovery has handled this work), and the referral adds a referral cost recovery fee — a percentage surcharge on top of everything you already owe.

- Active enforcement. Bank levies, wage executions, and seizure of business assets become available, and the NJ SOIL program intercepts your state refunds and property-tax relief payments until the balance is gone.

- The long tail. A New Jersey judgment is generally enforceable for 20 years and can be renewed. Interest compounds the whole time, and the public record blocks mortgages, refinances, and many rental and licensing checks until it's satisfied.

Notice what's missing from that sequence: an equivalent of the IRS's pre-levy hearing. Once the COD exists, New Jersey doesn't owe you another formal warning cycle before it enforces — which is why "I'll deal with it when the next letter comes" is a worse strategy here than it is with federal debt.

Facing a levy over a New Jersey certificate of debt?

Once a COD is docketed, enforcement can start without another hearing — and interest plus collection fees are growing your balance right now. Send us the certificate or your Division of Taxation notice and an experienced tax professional will map your fastest way out. Free, confidential, no pressure.

How to remove a certificate of debt in NJ: your options

Every certificate of debt comes off the docket the same way — the Division of Taxation files a warrant of satisfaction with the Superior Court once the underlying debt is resolved. The real question is which resolution path gets you there. (For the general mechanics of negotiating a tax balance, see our guide to how to settle tax debt yourself — this section covers only what's specific to New Jersey.)

| Option | Best for | Key requirement | Effect on the COD |

|---|---|---|---|

| Pay in full | Balances you can cover now | Funds available; get an exact payoff figure first | Warrant of satisfaction filed; judgment cleared |

| Installment agreement | Steady income, can't pay at once | Stay current on new taxes; financial details at higher balances | Enforcement typically pauses; COD stays on record until paid |

| Closing agreement (compromise) | Genuine inability to ever pay in full | Documented proof that full collection is unrealistic | Reduced payoff, then satisfaction filed |

| Hardship deferral | No ability to pay anything now | Financial documentation; reviewed case by case | Enforcement can pause; interest keeps accruing |

| Contest the assessment | Estimated or incorrect assessments | Actual returns or proof of error; act quickly | Judgment reduced or vacated if the assessment is corrected |

| Bankruptcy (rare fit) | Older income-tax years with broader debt problems | Legal advice — timing rules are strict | Personal liability may go; the docketed lien can survive |

Costs and timelines differ sharply between these paths, and the biggest cost driver is one most people don't see coming: the collection-referral surcharge. Resolving before referral is meaningfully cheaper than resolving after.

| Option | Cost to start | Ongoing cost | Typical timeline |

|---|---|---|---|

| Pay in full | Full balance plus fees and interest to date | None once satisfied | Satisfaction typically recorded within weeks of payoff |

| Installment agreement | Often a down payment; no large application fee | Interest continues on the unpaid balance | Can be set up in days; months to years to pay out |

| Closing agreement | No set fee, but heavy documentation of finances | None once accepted and paid | Months of Division review; no guaranteed outcome |

| Contest / file real returns | Cost of preparing accurate returns | Interest on whatever balance survives | Weeks to months for the Division to re-figure the account |

| Hardship deferral | Documentation only | Interest accrues the entire time | Reviewed periodically; not a permanent fix |

What $68,500 in New Jersey debt actually looks like

This example is hypothetical, but the arithmetic is the arithmetic. Say you owe New Jersey $68,500 and the COD has been docketed. If the account gets referred to the state's collection contractor, the referral cost recovery fee — effective June 15, 2026 the state's new collection contractor charges 9.85% (previously 11%); the fee is set by the collection contract and changes, so confirm the current figure with the Division — adds roughly $68,500 × 9.85% ≈ $6,750, pushing the balance to about $75,250 before another day of interest.

Spread over a hypothetical 60-month payment plan, that's roughly $75,250 ÷ 60 ≈ $1,254 per month, before ongoing interest. Resolve the same debt before referral and the base math is $68,500 ÷ 60 ≈ $1,142 per month — the referral alone costs about $6,750, more than a year's worth of the difference between the two payments. And if two of the years behind that $68,500 were estimated assessments for returns you never filed, filing the real returns could cut the principal before you ever negotiate a payment. Order of operations is everything here: correct the number first, then arrange to pay it.

Where the debt came from matters too. Atlantic City W-2G winnings that were never fully reported create both a federal and a New Jersey problem — see casino winnings tax debt — and online sellers can pick up New Jersey sales-tax exposure without realizing it, a pattern covered in Amazon FBA seller taxes. Business trust-fund taxes like sales tax get less flexibility from the Division than personal income tax, so the resolution path shifts with the tax type.

NJ certificate of debt vs. an IRS tax lien: not the same animal

A certificate of debt is more aggressive than its federal counterpart in almost every dimension that matters. If you owe both New Jersey and the IRS, this comparison usually decides the sequencing — our guide on state tax debt vs IRS works through which to resolve first. New York's version of the same tool is a New York tax warrant, and it behaves similarly.

| Feature | NJ certificate of debt | IRS collection |

|---|---|---|

| How it's created | Administrative docketing with the Superior Court; no lawsuit | Federal tax lien arises by statute; levy only after a final notice |

| Hearing before enforcement | None at docketing — the protest window was ~90 days after assessment | Collection Due Process rights: 30 days after LT11/Letter 1058 to request a hearing |

| How long it lasts | Judgment generally enforceable 20 years, renewable | 10-year collection statute (CSED), extendable by tolling events |

| Refund offsets | SOIL intercepts NJ refunds and property-tax relief | Federal refunds applied to the balance until paid |

| Settlement path | Case-by-case closing agreement; no standardized program | Offer in Compromise: formal program, $205 fee, published criteria |

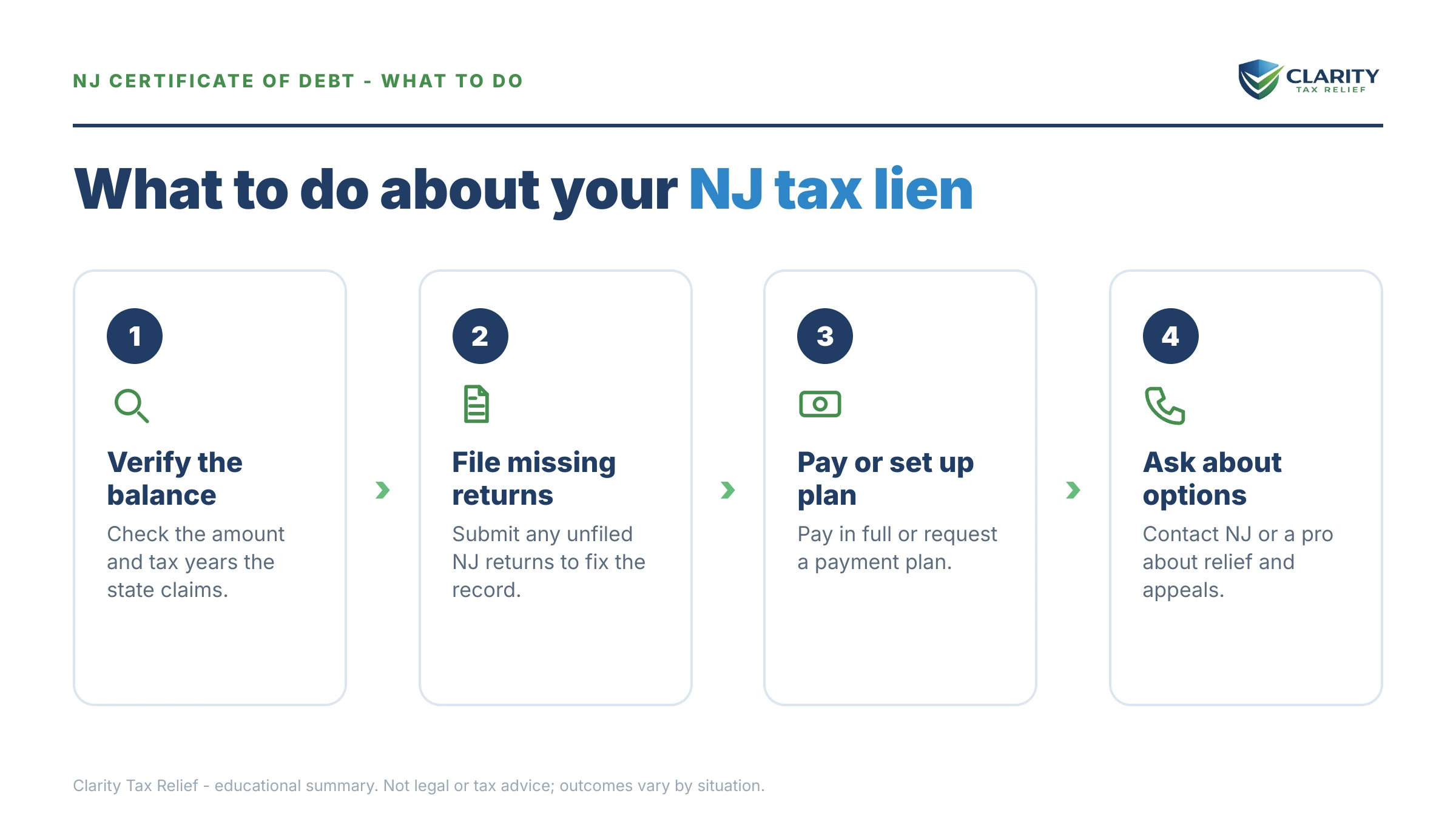

How to respond to a NJ certificate of debt, step by step

- Pull the docket details. Get the docket number, judgment amount, and tax periods from the certificate or from the Division of Taxation so every later call references the right record.

- Verify the balance behind it. Request an account breakdown by year; if any period was estimated because you never filed, filing the actual return can shrink the judgment dramatically.

- Contact the Division before enforcement does. Call the Division of Taxation — or its collection contractor, if your account was referred — and get a resolution in motion before a bank levy or wage execution issues.

- Choose your resolution path. Pick payment in full, an installment plan, a closing agreement, or a challenge to the assessment based on your finances and how the debt arose.

- Confirm the warrant of satisfaction. After payoff, verify the Division filed the satisfaction with the Superior Court and keep certified copies for lenders, landlords, and title companies.

When you can handle this yourself — and when help changes the outcome

Plenty of certificate-of-debt situations don't need professional help. If the balance is one you can pay in full, or it's a single accurate year and you just need a payment plan, call the Division, set it up, and confirm the satisfaction afterward — that's a phone-and-paperwork task, not a case. The same goes if the COD reflects a payment that simply never posted: send proof and follow up.

Experienced help earns its cost in four situations: a levy or wage execution is already in motion and needs to be intercepted before payday; multiple years are unfiled and the judgment is built on estimated assessments that have to be unwound in the right order; the debt is business sales or payroll tax, where personal liability and trust-fund rules raise the stakes; or you're pursuing a closing agreement, where the financial presentation decides whether the Division engages at all. In those cases the difference isn't convenience — it's the final number and how fast enforcement stops.

Terms on your certificate of debt, decoded

- Certificate of debt (COD): the document the Division of Taxation files with the Superior Court that turns an unpaid assessment into a judgment without a lawsuit.

- Docketed judgment: a judgment entered on the Superior Court's statewide record — the status that creates the lien and unlocks enforcement tools.

- Warrant of satisfaction: the court filing that marks the judgment paid and clears the COD from the docket.

- Referral cost recovery fee: the percentage surcharge New Jersey adds when a docketed debt is referred to its private collection contractor.

- SOIL (Set-Off of Individual Liability): New Jersey's program for intercepting your state refunds and property-tax relief payments to pay the debt.

- Closing agreement: New Jersey's case-by-case mechanism (N.J.S.A. 54:53-1) for settling a tax debt for less than the full balance — its rough equivalent of an IRS Offer in Compromise.

NJ certificate of debt questions, answered

What is a certificate of debt in New Jersey?

A certificate of debt is a document the New Jersey Division of Taxation files with the Clerk of the Superior Court that carries the same force as a civil judgment against you. No lawsuit or hearing happens first — it is an administrative filing. Once docketed, it creates a lien on property you own in New Jersey and lets the state use judgment-enforcement tools like wage executions and bank levies.

How do I remove a certificate of debt in NJ?

Resolve the underlying tax — by paying, negotiating, or correcting the assessment — then make sure the Division files a warrant of satisfaction with the Superior Court. Confirm the filing yourself and keep certified copies for lenders and title companies. If the assessment behind the certificate is wrong, such as an estimated assessment for a year you never filed, filing the actual return or contesting the figures can shrink or eliminate the judgment.

Does a NJ certificate of debt expire?

Not on the IRS's timetable. A docketed certificate of debt works like a New Jersey judgment, which is generally enforceable for 20 years and can be renewed, and interest keeps accruing the entire time. Waiting it out is not a realistic strategy for New Jersey debt the way the federal 10-year collection statute sometimes is for IRS debt.

Does a certificate of debt show up on my credit report?

The three major credit bureaus stopped reporting tax liens and civil judgments in 2018, so it will not appear as a tradeline. But it is a public court record: mortgage lenders, landlords running background checks, and title companies routinely find it in public-records searches, and it can sink a home purchase, refinance, or rental application until it is satisfied.

Can New Jersey levy my bank account or garnish my wages with a certificate of debt?

Yes. Once the certificate is docketed, the Division of Taxation can enforce it the way a judgment creditor would — reaching bank accounts, wages, and other assets — and it can intercept your state refunds through the SOIL program. Renting does not insulate you: the judgment does not need real estate to attach to before the state pursues your income and accounts.

Can I settle a NJ certificate of debt for less than I owe?

Sometimes, through a closing agreement — New Jersey's narrow equivalent of an IRS Offer in Compromise. There is no standardized application-and-fee program; the Division negotiates case by case and expects documented proof that full payment is genuinely beyond your means. Most people with steady income resolve a certificate of debt through a payment plan instead.

Is a call from Pioneer Credit Recovery about New Jersey taxes legitimate?

Usually, yes — New Jersey refers docketed tax debts to a contracted private collection agency, and Pioneer Credit Recovery has handled that work. Verify before paying anything: contact the Division of Taxation directly and confirm the balance, and never pay by gift card, wire transfer, or payment app. Be aware that the referral itself adds a cost recovery fee on top of your balance.

Why didn't I get a court hearing before the certificate of debt was filed?

Because the statute does not require one. N.J.S.A. 54:49-12 lets the Division docket a certificate of debt administratively once an assessment becomes final. Your chance to be heard came earlier — generally a 90-day window to protest the assessment or petition the Tax Court of New Jersey — which is why final assessment notices matter so much and why estimated assessments should never be ignored.

Your next 24 hours

- Find the docket number and judgment amount on the certificate or your Division of Taxation letters — every call about this account starts with those two items.

- Gather your last filed New Jersey return, the assessment notices behind the COD, and your current income and bank information — that's everything needed to compare the judgment against reality and price a payment plan.

- Get a free case review — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779. With a docketed judgment, enforcement needs no further warning and interest plus collection fees are compounding; every week you wait resolves against a bigger number.

You can verify anything in this guide against the primary sources: the New Jersey Division of Taxation publishes its collection and judgment procedures, and docketed judgments are records of the New Jersey Courts. When a state-specific figure matters to your case — the current referral fee rate, plan terms, interest rate — confirm it with the Division directly rather than relying on any secondary source, including this one.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.