IRS Data Study

How Many People Are on IRS Payment Plans? Installment Agreement Statistics (2026)

The short answer: in fiscal year 2025, the IRS had about 4.87 million installment agreements active in its ending inventory — meaning roughly 4.87 million taxpayers were on IRS payment plans. That was up from about 4.64 million the year before. A payment plan is the IRS's most common way to resolve a balance you can't pay all at once.

Not sure which payment plan fits your balance?

An experienced tax professional can review your situation and explain your options — which plan you may qualify for, and what it would cost you. The consultation is free, confidential, and no-pressure.

Key findings: IRS payment plan statistics (FY2025)

- About 4.87 million taxpayers were on IRS payment plans at the end of fiscal year 2025 — the active installment agreements in the IRS's ending inventory.

- That total grew year over year, rising from about 4.64 million in fiscal year 2024 to about 4.87 million in fiscal year 2025.

- The IRS set up about 3.16 million new installment agreements in fiscal year 2025 — down from about 3.40 million new agreements in fiscal year 2024.

- The IRS collected about $17.9 billion through installment agreements in fiscal year 2025, up from about $16.1 billion the year before.

- About 1.96 million taxpayers fully paid off their installment agreements, finishing their balance through a payment plan.

The full data: IRS installment agreements, FY2024 vs. FY2025

Here is how the numbers compare across the two most recent fiscal years, drawn directly from the IRS Data Book. All figures are rounded.

| Measure | FY2024 | FY2025 | Change |

|---|---|---|---|

| Active installment agreements (ending inventory) | ~4.64 million | ~4.87 million | Up ~230,000 |

| New installment agreements established | ~3.40 million | ~3.16 million | Down ~240,000 |

| Dollars collected through installment agreements | ~$16.1 billion | ~$17.9 billion | Up ~$1.8 billion |

What this means in plain English

If you owe the IRS and can't pay in full, you are far from alone. Nearly 4.9 million people were paying down a tax balance on a monthly plan at the close of fiscal year 2025. That makes the IRS payment plan the single most common way taxpayers resolve a debt they can't clear in one check.

A few things stand out in the data:

- More people are on plans than ever. The active total rose by roughly 230,000 in a single year. As balances and interest grow, more taxpayers turn to monthly agreements.

- Fewer new plans, but more dollars collected. The IRS opened fewer new agreements in FY2025 yet collected about $1.8 billion more through them. That points to larger balances and steady payments on existing plans.

- Plans work when you stick with them. About 1.96 million agreements were fully paid off — proof that a payment plan is a real path to finishing a tax debt, not just delaying it.

The practical takeaway: setting up a payment plan is normal, routine, and something the IRS approves for millions of people every year. It stops the collection notices from escalating while you pay the balance down over time. Keep in mind that interest and the failure-to-pay penalty (generally 0.5% of the unpaid tax per month) keep adding up until the balance hits zero — you can estimate that running cost with our IRS penalty and interest calculator.

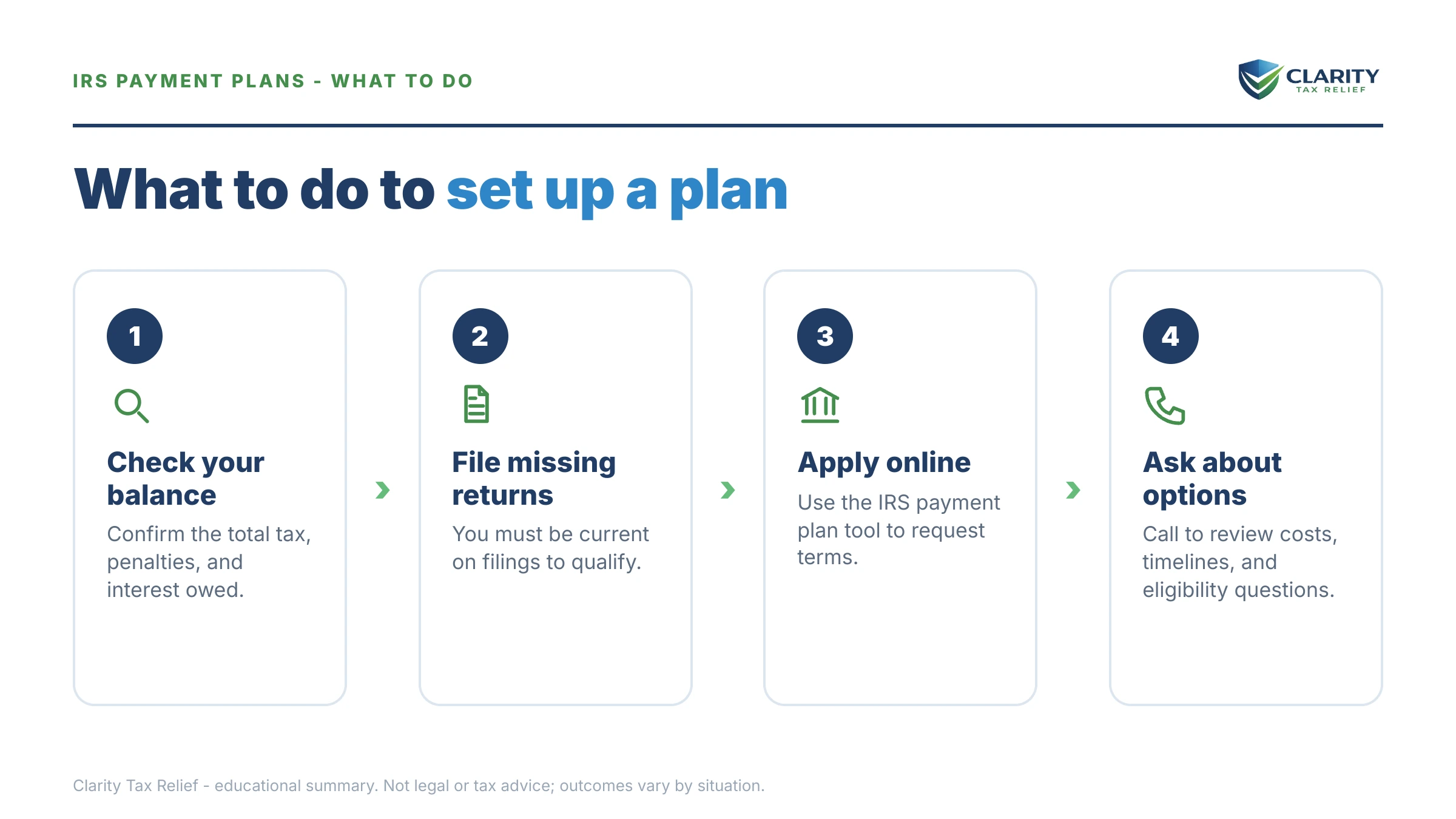

The two types of IRS payment plan

"Installment agreement" is the official name for a payment plan. There are two main kinds:

- Short-term payment plan. Gives you up to 180 extra days to pay the full balance. There's no setup fee, though interest and penalties continue.

- Long-term installment agreement. A monthly plan, usually spread over up to 72 months. For balances under about $50,000, a "streamlined" agreement can often be set up without handing over detailed financial records.

You can apply online, by phone, by mail, or in person. The IRS explains the full process and current fees on its payment plans and installment agreements page. If you'd rather request one by letter, our guide on the IRS installment agreement request letter walks through exactly what to write.

Methodology & source

All figures in this study come directly from the IRS Data Book, Fiscal Year 2025, Table 4-1 (Delinquent Collection Activities), published by the IRS. The IRS reports on a federal fiscal year, which runs October 1 through September 30. "Ending inventory" counts installment agreements still active at the end of the fiscal year; "established" counts new agreements opened during the year. We rounded the published figures for readability and have not adjusted, projected, or estimated any numbers beyond what the IRS reported.

Primary source: IRS Data Book, Table 4-1 — Delinquent Collection Activities. For more IRS data breakdowns, see our IRS tax studies hub.

Cite this study

Free to share or reference. Please credit Clarity Tax Relief with a link back to this page.

Attribution line:

Clarity Tax Relief, "How Many People Are on IRS Payment Plans? Installment Agreement Statistics (2026)." Source: IRS Data Book FY2025, Table 4-1. How Many People Are on IRS Payment Plans? Installment Agreement Statistics (2026)

Frequently asked questions

How many people are on IRS payment plans?

In fiscal year 2025, the IRS had about 4.87 million installment agreements in its ending inventory — meaning roughly 4.87 million active payment plans. That was up from about 4.64 million the year before. A payment plan, also called an installment agreement, is the most common way taxpayers resolve a balance they can't pay all at once.

How much money does the IRS collect through payment plans?

The IRS collected about $17.9 billion through installment agreements in fiscal year 2025, up from about $16.1 billion in fiscal year 2024. These are dollars paid by taxpayers who owed a balance and chose to pay it over time rather than all at once.

How many new IRS payment plans are set up each year?

The IRS established about 3.16 million new installment agreements in fiscal year 2025, down from about 3.40 million in fiscal year 2024. New agreements are different from the total ending inventory, which counts every plan still active at the end of the year.

What types of IRS payment plans are there?

There are two main types. A short-term payment plan gives you up to 180 extra days to pay in full. A long-term installment agreement lets you pay monthly, usually over up to 72 months. For balances under about $50,000, a streamlined agreement can often be set up without detailed financial disclosure.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.